As part of our work analysing the UK’s regional FinTech ecosystems the team at Whitecap has spent a lot of time collecting and studying FinTech data, and we are constantly on the lookout for new data points to help gauge the development of the FinTech sector. This is our second blog about the Kalifa Review, you can read the first one here.

These are the 10 key data points about UK FinTech we noted in the Kalifa Review:

-

With 10% of global market share and generating £11bn in revenue, the UK is a dominant force in FinTech.

-

There are an estimated 2500 FinTech firms in the UK (81% of which are made up of less than 50 people) and they have an annualised growth of 16% vs the SME average of 1.3%.

-

FinTech’s £11bn contribution to the economy represents 8% of the UK’s financial services output, and is estimated to rise to £13.7bn GVA by 2030, with job creation contributing to 70% of this.

-

Investment into UK FinTech stood at $4.1bn in 2020 – more than the next 5 European countries combined, and in 2021 over $1bn of investment had already been committed to UK FinTech within the first two months.

-

Better connectivity has the potential to uplift GVA by between £2.4 and £3.0bn, and create a 50% increase in FinTech jobs.

-

The total tech spend by UK financial services firms was £95bn in 2019, including SMEs and corporates.

-

97% of FinTech founders have used tax-incentivised investment schemes including EIS, Seed Enterprise Investment Scheme (“SEIS”) and VCT.

-

67% of the UK’s fastest growing FinTechs consider talent to be a high priority.

-

In 2020, 43% of job adverts from UK FinTech scaleups were seeking data skills, 44% technology skills and 35% business skills.

-

UK citizens are becoming increasingly digitally active and 71% are now using the services of at least one FinTech company.

These data points are drawn from a range of sources, all of which are cited in the Review, and include analysis from KPMG, EY, Deloitte, and Innovate Finance, in addition to research commissioned as part of the Review.

Mapping the national FinTech sector

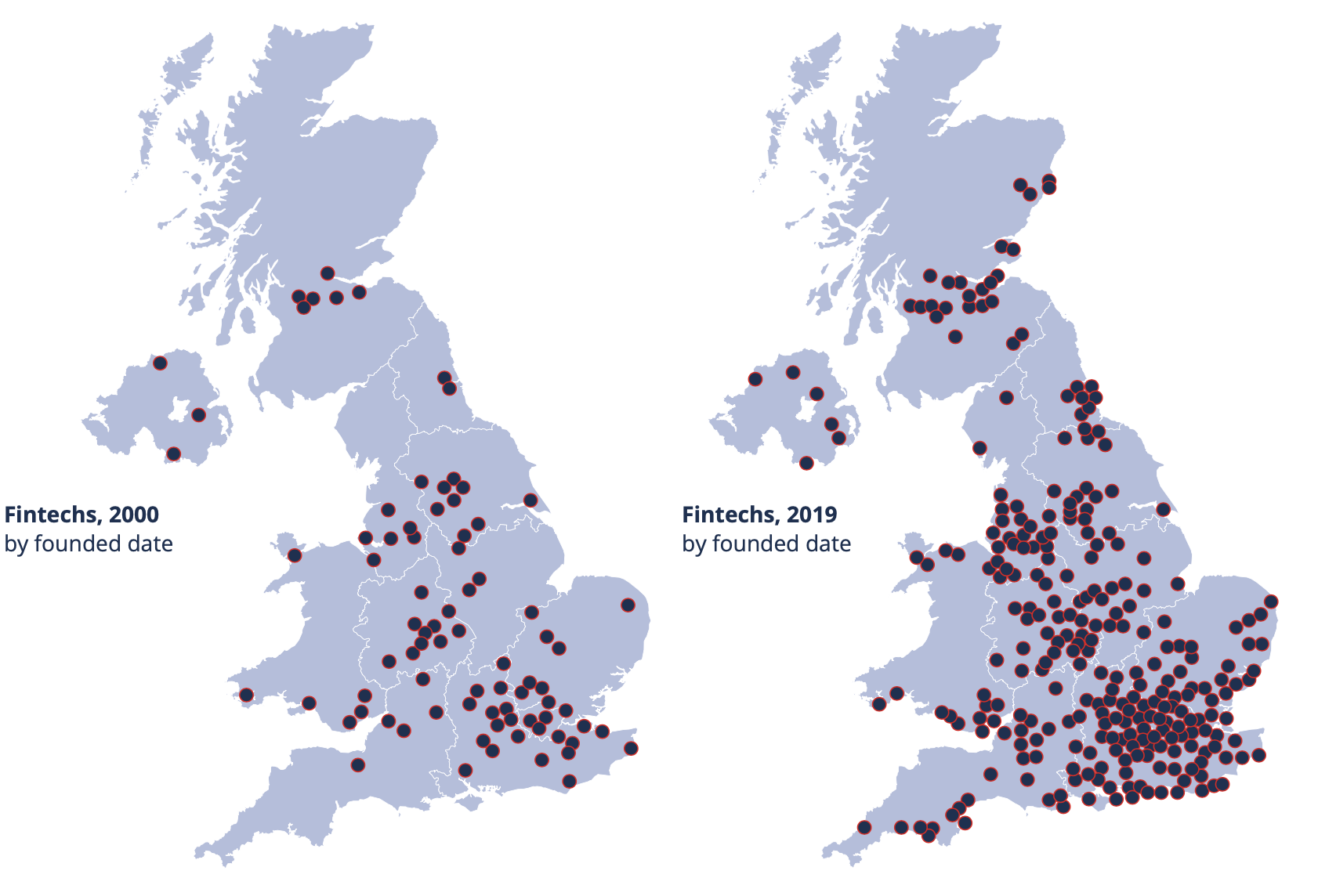

Deloitte’s analysis of the FinTech sector in the UK, conducted for the Kalifa Review as part of the National Connectivity chapter, identifies an estimated 2500 firms. Around two thirds of these FinTechs are now estimated to be headquartered in London, but even before Covid there was increasing evidence of FinTech firms expanding their footprint from the capital into other cities. Deloitte used a combination of big data, AI and supporting research to complete its analysis and form a national view, and the visual below illustrates how the sector has developed since 2000:

The Review states:

“UK fintech has seen consistent growth in the UK since 2000 to a total of c.2,500 fintech companies today, with a period of stronger growth during 2011-2016, when the number of fintechs increased 16-21%, year on year. There are signs that the rate of growth has slowed in recent years, but there’s still plenty of activity throughout the country, albeit grouped together in clusters.”

The challenges with FinTech data

The data points points listed above provide a useful summary of the national FinTech sector, and new data on the sector is always welcome. The new national data was used to identify the top 10 regional clusters in the Review. Unsurprisingly the new data has led to considerable discussion around the regional FinTech community and it would be very interesting to see the broken down regional data at company level. This is undoubtedly a challenging sector to measure, and the lack of standardised data relating to FinTech is highlighted in the Review:

“During the course of the review there has been extensive data cleansing of a number of current data sources to establish an accurate picture of UK fintech. For example, research found that over 50% of fintechs are unable to classify themselves (including the likes of Monzo, Wise, Funding Circle, Revolut, etc.) using the current Standard Industrial Codes (SIC 2007). Thus repeatable, accurate analysis on the fintech industry by the ONS, government and other interested parties is not currently possible and there is a need to establish a platform that enables liquidity of information.”

The need for up to date data and the difficulties of analysing and classifying FinTech firms and jobs are topics we wrote about in detail in our April 2020 blog: How do you measure FinTech? (and why should we care?). The limitations of SIC codes is a known issue and one that is already being tackled. The Data City has recently written a blog in response to the Kalifa Review, outlining its work addressing the challenge of the lack of relevant SIC codes.

Our own analysis of regional FinTech has looked at specific regions one at a time. Whitecap has analysed 6 regions, all of which are part of the top 10 clusters highlighted in the Review, including Leeds City Region, Greater Manchester and West Midlands, which are part of the ‘established’ clusters identified. We have also analysed the ’emerging’ clusters in the North East, Bristol & Bath and Northern Ireland. Across this analysis, we have deployed a standard approach to the classification of firms involved in FinTech, and have used primary research to identify and validate each individual FinTech firm. We identified approximately 150 active FinTech startups and scaleups across these six regions between 2019-20, 82% of which were headquartered within the region we researched. Not all FinTech firms are startups and scaleups of course, but when reviewing larger or more established firms it becomes extremely subjective as to whether all, the majority or just part of their operations can be classed as FinTech. There is also the issue of tech firms who develop FinTech solutions for the FS sector, but also work across other sectors. Overall, our analysis identified almost 600 firms estimated to be operating in the FinTech sector within the 6 regions we have researched, but not all of these firms would class as FinTechs in their own right. All of these firms and their categorisation are individually named in our reports, and our methodology has been published within the individuals reports and a blog.

Why is FinTech data important?

The need for accurate data to help support the development and promotion of the UK’s FinTech sector is something we articulated in our blog last year, when we said:

“As the UK continues to develop its FinTech capability and invest in the future of the sector, it would be prudent to be able to call on some up to date industry statistics to help the many strong supporters of the sector tell a compelling story on a regional, national and international basis.”

The Review highlights that this data is not only useful for analysis and promotion of the sector, but also for the FinTech firms themselves:

“Strategic national coordination, combined with accurate, openly accessible, national data will give UK FinTechs access to the key ingredients that are indicative of success and growth – talent, investment, partnerships, and expertise from industry peers.”

We fully support this statement and hope to see industry data at the heart of the objectives for the proposed new national Centre for Finance, Innovation and Technology (CFIT). How this data is collated and maintained will be critical, and it will be important to find the right balance across the data collection options available. Clearly there is a degree of subjectivity around how the sector is measured, which is unsurprising given the difficulties in identifying and classifying FinTech firms. Having an industry standard way to identify FinTech firms would be extremely helpful, and we were encouraged to see the Review highlight the difficulties the sector faces and call for a platform to enable accurate analysis.

You can read more of our thoughts on the Review in our recent blog, The Kalifa Review – Regional FinTech reflections.

If you’d like to discuss this blog post or share your own perspective on the issues covered, please get in touch or comment via our social media channels on LinkedIn or Twitter.

Established in 2012, Whitecap Consulting is a regional strategy consultancy headquartered in Leeds, with offices in Manchester, Milton Keynes, Birmingham, Bristol and Newcastle. We typically work with boards, executives and investors of predominantly mid-sized organisations with a turnover of c£10m-£300m, helping clients analyse, develop and implement growth strategies. Also, we work with clients across a range of sectors including Financial Services, Technology, FinTech, Outsourcing, Consumer and Retail, Property, Healthcare, Higher Education, Logistics, Manufacturing and Professional Services, including Corporate Finance and PE.