There was much to digest in the highly-anticipated Kalifa Review published on Friday 26th February. Whitecap’s deep involvement in the analysis and development of regional FinTech capability and ecosystems over recent years meant the regional implications were our primary area of interest. This is our first blog on this topic, read the second one here.

There was much to digest in the highly-anticipated Kalifa Review published on Friday 26th February. Whitecap’s deep involvement in the analysis and development of regional FinTech capability and ecosystems over recent years meant the regional implications were our primary area of interest. This is our first blog on this topic, read the second one here.

The inclusion of regional FinTech in the scope of the Kalifa Review had long been known, and was represented in the National Connectivity chapter, one of five workstreams along with Policy and Regulation, Skills and Talent, Investment, and International Attractiveness and Competitiveness. The National Connectivity workstream was led by Tech Nation, who have summarised their findings in a useful post here. This chapter is even more relevant today than it was in March 2020 when the Chancellor first announced the intention to conduct the Review; before Covid led to the first national lockdown and an extension to the timeline for the Review. Since that time, the move to a remote working model has highlighted that geography need not be the barrier it previously was considered to be in key areas such as employment, access to market, and the ability to engage with investors. Consequently, ‘levelling up’ in FinTech is no longer simply an aspiration – it’s a work in progress.

Whitecap had the opportunity to feed the outputs of our regional FinTech analysis reports into the data gathering process. Across our six regional locations (all of which are outside London) we are well connected into the regional and national FinTech sector via our client work with FS, tech and FinTech organisations. We have also been involved in creating and coordinating two regional ecosystem bodies: FinTech North and FinTech West. Both of these organisations are part of the FinTech National Network, which is coordinated by Innovate Finance (also secretariat on the Kalifa Review) and also includes FinTech Scotland, FinTech Wales, FinTechNI and the recently formed SuperTech WM cluster in the West Midlands. Additionally, Chris Sier, Chair of FinTech North, Treasury FinTech Envoy, and a long-standing advocate of regional FinTech, was a member of the National Connectivity chapter.

Regional Clusters

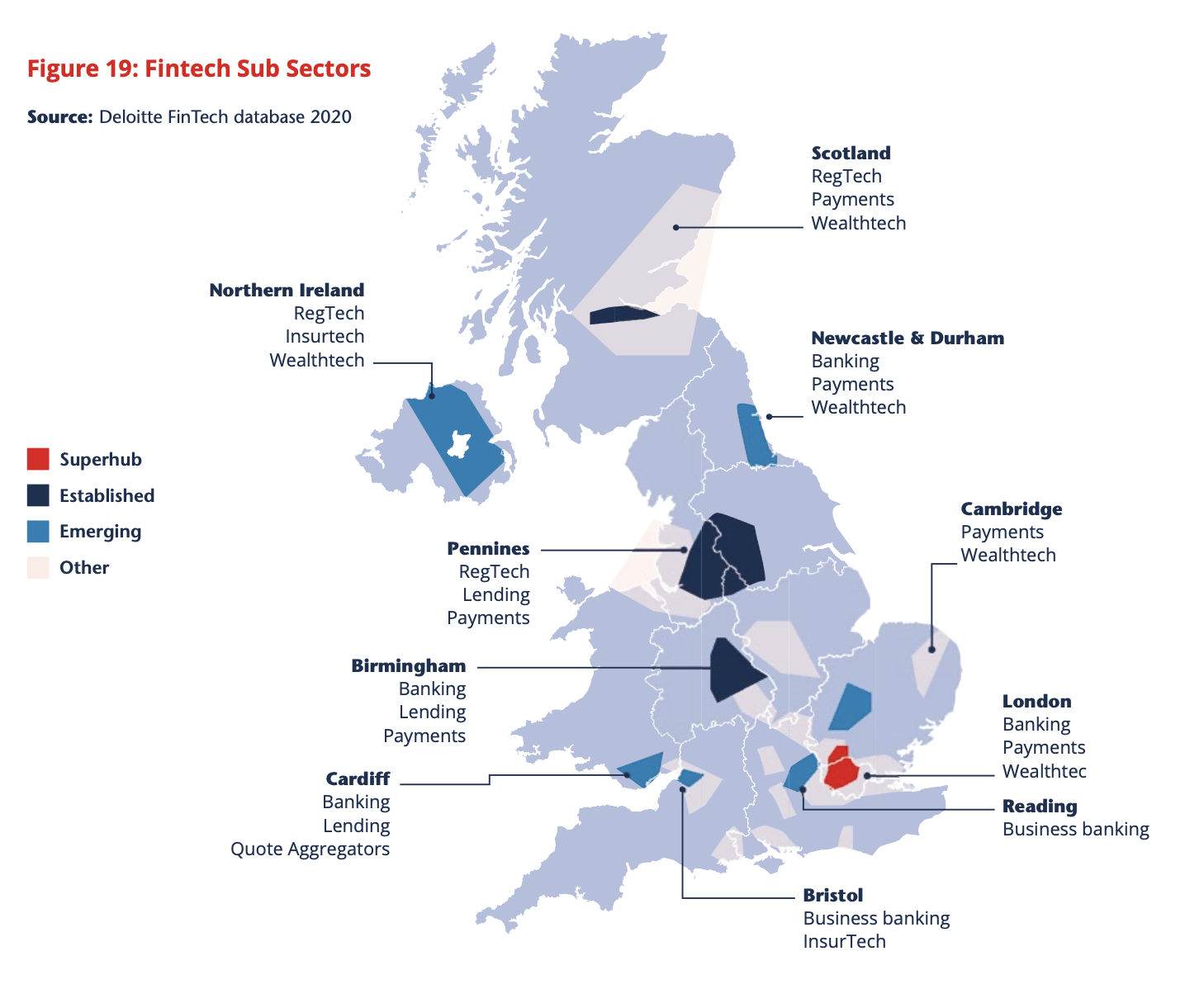

From a regional FinTech perspective, the main headline from the Review was the identification of 10 key clusters across the UK. These clusters, which have been identified using data relating to the locations of FinTech firms, are a mixture of cities, regions and countries. Ranked in order, these clusters have been identified as:

- London

- Manchester & Leeds (currently badged as ‘The Pennines’ in the Review)

- Scotland (especially the Edinburgh / Glasgow corridor)

- Birmingham

- Bristol & Bath

- Newcastle & Durham

- Cambridge

- Reading & West of London

- Wales (especially Cardiff & South Wales)

- Northern Ireland

London is a ‘super cluster’, Manchester & Leeds, Scotland and Birmingham are labelled ‘established’, and the other clusters are ’emerging’. Analysis undertaken for the Review identified 25 clusters of FinTechs across the UK, which are at different stages of growth and development, with different focus areas and specialisms. 10 clusters were found to be producing high growth FinTechs (c10% of FinTechs achieving high-growth status) and to have the most potential to grow and develop further.” The Review highlights some of the strengths of each cluster via the graphic below:

So the data has identified 10 key clusters, but what happens next? Who is responsible for these clusters? What infrastructure and resources (if any) will they have? Clearly there is existing activity in all these regions, including networks, communities and elements of governance, not to mention the Treasury’s network of FinTech Envoys who provide a direct link to London. Much of this activity will already be aligned to the themes of the Review, but the recommendations make new asks of the regions.

So the data has identified 10 key clusters, but what happens next? Who is responsible for these clusters? What infrastructure and resources (if any) will they have? Clearly there is existing activity in all these regions, including networks, communities and elements of governance, not to mention the Treasury’s network of FinTech Envoys who provide a direct link to London. Much of this activity will already be aligned to the themes of the Review, but the recommendations make new asks of the regions.

One of the recommendations of the Review is that each of the 10 clusters should develop a 2-3 year strategy for development. At this stage it is not known where the ownership of creating these strategies will sit, or how their production and subsequent actions will be resourced or funded. One possible clue lies in this wording within the recommendations: ‘Secure funding to support its implementation e.g. LEPs or City Deals where these are available’. For some regions this may create a remit that is clearer than for others, as not all the clusters fall directly into distinct areas covered by Local Authorities, Local Enterprise Partnerships (LEPs) or City Deals, or devolution deals. This is a grey area that for many regions will require clarification before any action will be taken.

However a 2-3 year strategy is developed, what is clear is that what has already been created, either with or without a strategy, needs to be nurtured and developed; not overwritten. Organisations such as FinTech North, FinTech West, FinTech Scotland, FinTech Wales, FinTechNI and SuperTech WM are all existing entities with their own unique approaches. For example, Fintech North, the first of the regional networks, was created in 2016 and has been grown organically with only vocational governance and no central funding. Having built a community of 4000+ people and run nearly 80 FinTech focused events, it is widely considered to be an open and accessible forum which adds value by bringing together the northern FinTech community. As a co-creator of Fintech North, we would not wish for its value be diminished by a need to conform to the practices of other regions or directives from a central overseeing organisation (such as CFIT – see below). FinTech West, which Whitecap also helps coordinate, operates on a similar basis in the South West and aspires to take a dynamic approach to supporting the development of FinTech community. These organisations are quite distinctive from some of the other networks which have been created with more public sector involvement from the outset. There are pros and cons in all the models in operation of course, but a key point here is that one size does not (and will not) fit all.

Another observation is that some of the 10 clusters are more geographically and structurally logical than others. The most notable example here is the Manchester & Leeds cluster, within which there are two significant FinTech hubs; each of which comes under a different local authority and inward investment organisation / LEP. Furthermore, the 45 miles between these two cities is notable primarily for the mountains and hills that lie between them (the Pennines), along with an unreliable train route and the congested M62 motorway. The data may point towards a single cluster, but the current reality is two very distinct ecosystems. To truly unite these two FinTech hubs would be a major achievement, and undoubtedly a very powerful one. The successful development of FinTech North over recent years has shown that cross-regional initiatives can prosper in terms of developing a joined-up northern FinTech community network (which also includes Liverpool, the North East and other parts of the north), but collaboration on areas such as economic development strategy remains relatively unproven and a challenging prospect.

Clearly there are a number of practical areas requiring clarification, and no doubt this will be forthcoming over the coming weeks and months as opinion and feedback is absorbed. We do not expect to see consistent widespread actions being taken in relation to the Review within the majority of the 10 clusters until this clarification is provided. That said, we do expect individual regions will start to put wheels in motion to support the growth of their FinTech clusters; a view that is supported by our conversations with various regional stakeholders across the UK since the Review was published.

Centre for Finance, Innovation and Technology (CFIT)

The Review recommends the creation of a national Centre for Finance, Innovation and Technology (CFIT). This may prove to be key to unlocking and delivering several recommendations across the report, not least for the National Connectivity chapter. Indeed, the narrative in the report indicates this will be the case:

“The Review states that CFIT will establish a set of specific deliverables, which indicatively could include target such as: increase the fintech adoption rate; increase the percentage of SMEs making use of external finance; double the number of UK domiciled fintech unicorns; increase the number of fintech listings on the London Stock Exchange, increase the number of fintech jobs; grow UK fintech market share. It would also be tasked with constructing and coordinating the UK National Fintech Connectivity Strategy, with responsibility for convening local and regional fintech leaders to develop and deliver the national strategy, working with stakeholders from across the UK to ensure national priorities draw on and support local capabilities.

The Centre will embed local strategies in its approach through consultation and data-sharing. It will also act as an information source, providing continuous insight, qualitative and quantitative, with mechanisms in place to deliver liquidity of information to all. It would also conduct research to inform decision-making, sector developments, and underpin future policy decisions. Additionally, CFIT will accelerate cluster specialisms, actively encouraging and increasing collaboration between industry and academia to double down on cluster strengths, with a priority on developing real-world commercial applications.”

This is clearly a broad and deep remit, and the creation of CFIT is one of the headline recommendations of the report, and its successful implementation would appear to be critical to enabling action to be taken in many areas across the Review.

From a national perspective, having strong regional representation within the leadership of CFIT will be crucial to ensuring the voices of the FinTech clusters and the wider ecosystem are heard. If this does not happen, there is the risk this will be seen as a London-centric initiative, and the regions may not engage.

There is already a risk of a perceived wish to centralise control via CFIT, and it is important this does not become the reality. From our own engagement with Ron Kalifa during the Review, we do not believe this is what he aspires to see. Part of the beauty and strength of the existing regional organisations is they have grown organically in response to demand. As an example, Fintech North remains independent from central or regional funding other than sponsorship. This has, of course, placed constraints on resourcing but has also resulted in a network that knows its constituents very well as funding has come from voluntary contributions. In other words, Fintech North only acts when demand is crystallised through sponsorship and support, rather than when policymakers ask it to. This agility and client-centred approach should not be lost through the centralisation of control that CFIT might represent. Other regional entities will wish to protect the foundations of their success too.

What next?

The Kalifa Review was commissioned as a strategic review of UK FinTech and has laid out a strategic plan for the development of the sector. This strategic plan is welcome, long anticipated and much needed. However, recommendations will not be delivered quickly, and the sector should not fall into the trap of watching and waiting for things to happen. There is much activity already in flow across the UK, and this has helped the sector to reach its current status as a global hub. The regional ecosystems (whether they are in the 10 clusters or not) need to continue to proactively progress their own development and to fly the flag for FinTech regionally, nationally and internationally. For the existing regional networks, it is business as usual until they can clearly understand what’s on offer and whether it aligns to their own objectives, values and the needs of their FinTech communities.

The publication of the Review is not the end, it is the end of the beginning. With an actionable plan in place that includes a clear mandate for each regional cluster along with the required resources and funding, we will be able to feel optimistic of meaningful actions resulting from the Kalifa Review.

From a Whitecap perspective, our interest, knowledge and passion in this field remains strong and we intend to play our role in the continued development of FinTech across the UK. We anticipate this will continue to involve, amongst other things: updating and enhancing our regional FinTech analysis work (including analysing additional regions); assisting with the development of FinTech development strategies for public and private sector organisations and higher education institutions; working with FinTech firms on their growth strategies and investment readiness; supporting FinTech investors by providing commercial due diligence on transactions; continuing to develop regional FinTech economies via our involvement in FinTech North and FinTech West; and by being vocal supporters and advocates for all the activity being delivered by many others across the UK.

This is our first blog on this topic, read the second one here.

_______________________________________________________________________________

Further reading – Overall & National Connectivity Recommendations

National Connectivity Chapter Recommendations

National Connectivity Chapter Recommendations

The National Connectivity chapter has three primary recommendations. For ease of reference, we have reproduced these recommendations in full below:

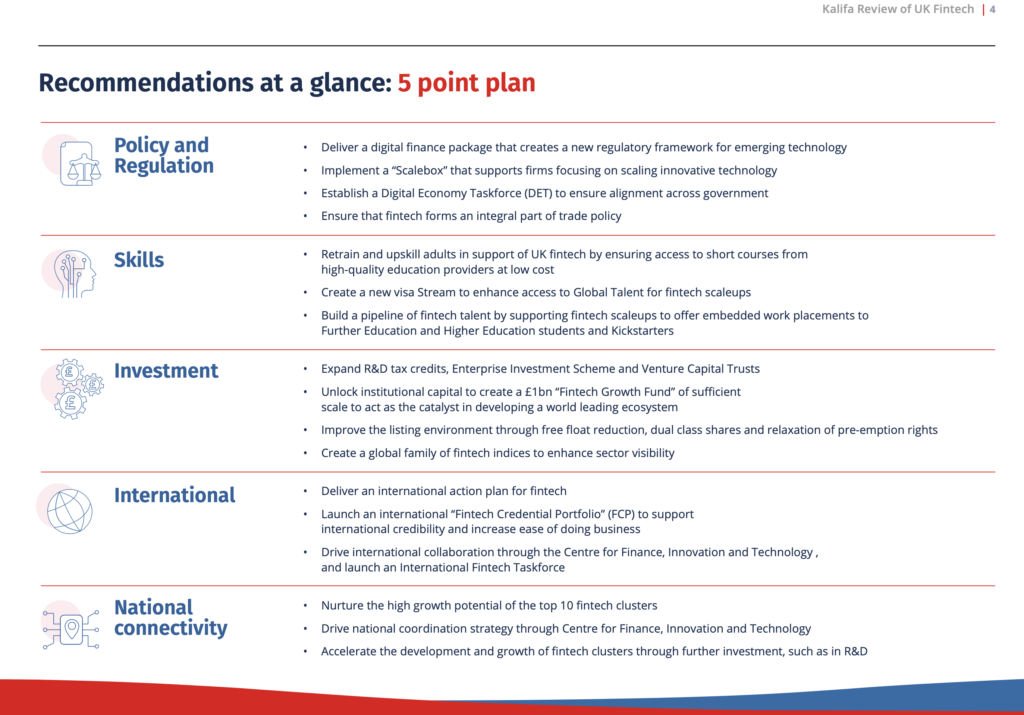

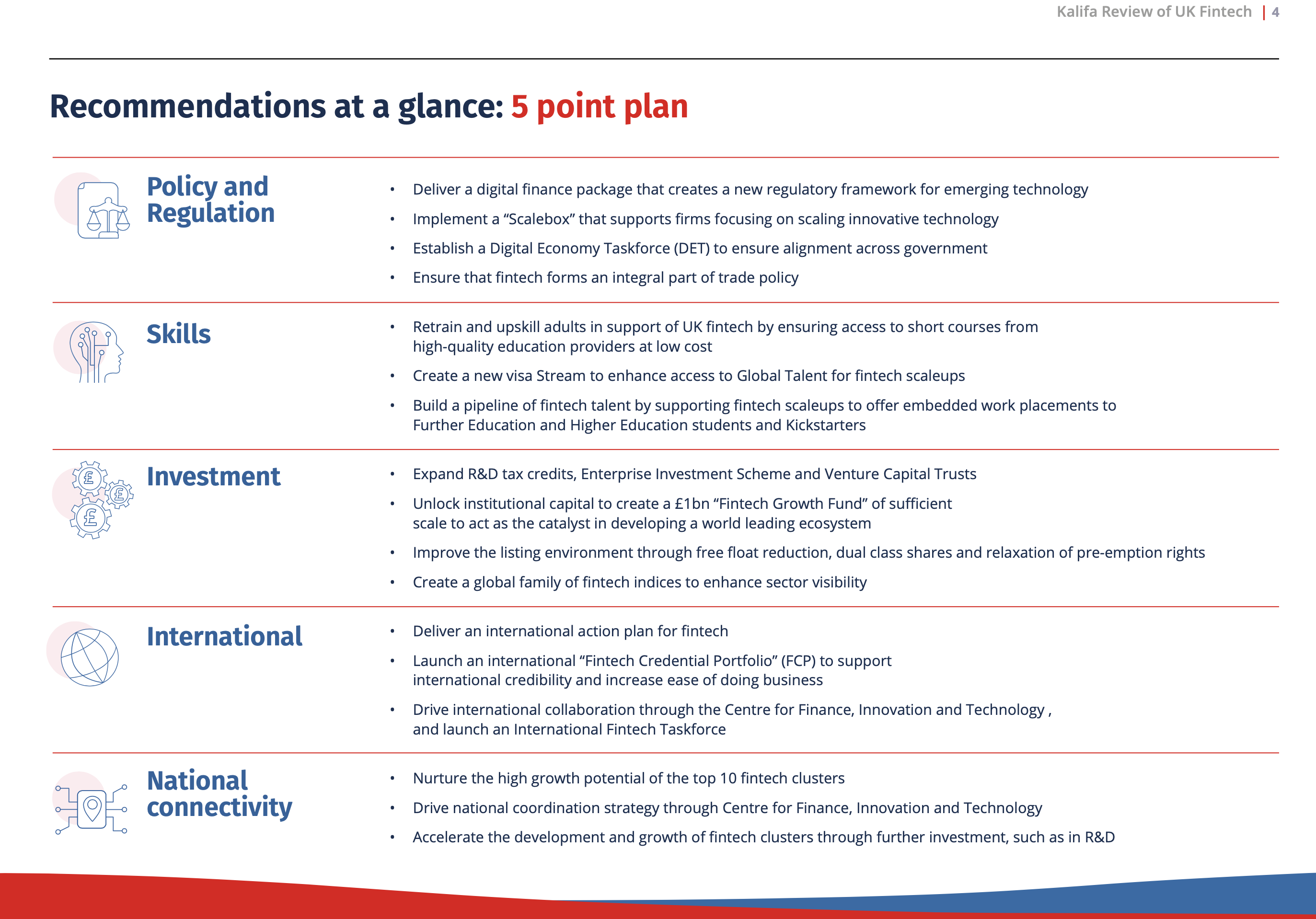

Recommendation 1

Nurture the high growth potential of the top 10 fintech clusters, with the proven foundational capabilities to optimise their particular areas of excellence.

Whilst this by no means seeks to disregard or discourage organic growth in wider areas, focusing efforts and available resources on these clusters is anticipated to create the strongest return at the fastest pace.

Each prioritised cluster to produce a three-year strategy to support their continued growth, foster specialist capabilities, and enhance national connectivity.

Cluster strategies should ideally:

- Be set against national baseline data.

- Be entrepreneur-focused (entrepreneur as the customer).

- Optimise identified areas of excellence and build on existing strengths.

- Secure funding to support its implementation e.g. LEPs or City Deals where these are available.

- Consider where cluster collaborations, both virtually and physically, might further support cluster goals.

Recommendation 2

Drive national coordination strategy through CFIT to ensure future fintech competitiveness and growth across the UK connectivity. This will deliver national coordination, with supporting data and technology infrastructure, to ensure future fintech competitiveness and growth across the UK.

CFIT should embed a data-led approach and maintain a national fintech database, which would provide open access data and ensure an evidence-based approach to sector developments.

To assist in its establishment, CFIT’s governing principles should include that it operates as a small central co-ordinating function with an Advisory Board comprising of public/private local/ regional representation, government/regulator and investor representation.

Primary objectives of CFIT should include:

Provide strategic cohesion of UK fintech ambition through facilitating national connectivity:

- present timely and regular research and insights into UK fintech through maintaining open, accessible sector data, to both understand, build on, promote and better co-ordinate UK fintech strengths and specialisms, both domestically and abroad.

- work with local/regional fintech leadership to drive connectivity of domestic networks in investment, talent, partnerships and academia.

- act as market and export knowledge hub for international opportunities.

Support UK fintech cluster development:

- assist in the establishment of commercially focused and investible governance models (where gaps exist).

- assist local leadership with development of three- year strategies through sharing of best practice and communicating national priorities.

- identify and disseminate innovation and/or geographical funding streams available to enhance UK fintech, assisting with bids to support clusters in accelerating their strengths and specialisms.

Recommendation 3

Accelerate the development and growth of fintech cluster excellence to take advantage of domestic opportunities and compete on global stage, through increasing research and development investment in the fintech sector.

In this regard CFIT should:

- identify and disseminate existing innovation and/or geographical funding streams available to enhance UK fintech.

- provide expert input to assist with industry-led bids to support clusters in accelerating their strengths, for example through fintech centres of Excellence, with an emphasis on commercial applications.

- liaise with Innovate UK on future plans to support fintech and professional services R&D, working together to evaluate and consider further routes for fintech innovation funding.

Strategic national coordination, combined with accurate, openly accessible, national data will give UK FinTechs access to the key ingredients that are indicative of success and growth – talent, investment, partnerships, and expertise from industry peers.

The UK’s clusters have evolved at differing speeds with different drivers, funding, organisational structures, governance, and approaches. They’ve used the foundational capabilities at their disposal to greater or lesser degrees. Some have grown independently in duplicative ways. This individual development reflects the different local support to FinTechs across the UK. The supporting bodies which represent fintech, and help them work together, vary in nature, purpose and resources.

This is the first of our blogs on the Kalifa Review, you can read the second one here: The Kalifa Review: 10 data points about UK FinTech

If you’d like to discuss this blog post or share your own perspective on the issues covered, please get in touch or comment via our social media channels on LinkedIn or Twitter.

Established in 2012, Whitecap Consulting is a regional strategy consultancy headquartered in Leeds, with offices in Manchester, Milton Keynes, Birmingham, Bristol and Newcastle. We typically work with boards, executives and investors of predominantly mid-sized organisations with a turnover of c£10m-£300m, helping clients analyse, develop and implement growth strategies. Also, we work with clients across a range of sectors including Financial Services, Technology, FinTech, Outsourcing, Consumer and Retail, Property, Healthcare, Higher Education, Logistics, Manufacturing and Professional Services, including Corporate Finance and PE.