In the recent budget the Chancellor announced a review of UK FinTech, to consider the support the government can provide to ensure “growth and competitiveness” in the sector. This is welcome news and comes at a time when FinTech in the UK is thriving.

Defining FinTech

What is a FinTech firm? How do you decide if someone works in FinTech? How do you measure the value generated by FinTech? These are some of the most commonly asked questions we hear in our work in FinTech, and they are hard to answer.

The definition of FinTech we use at Whitecap says it is ‘the application of technology to improve financial products and services’. This makes it a very broad category, in which it is acknowledged to be extremely challenging to categorise companies and jobs. There are no SIC codes via which to identify FinTech businesses, and there is no standard categorisation of what constitutes a FinTech job.

So FinTech is hard to measure, but why does that matter and why should we care? In simple terms, if FinTech is an important source of the UK’s current and future economic growth, then we need some accurate metrics around it. This will help inform regional and national decisions around strategy and investment, as well as providing a benchmark against which future progress can be measured.

Statistics such as the number of firms, number of jobs and economic value add (GVA) of the sector are headline figures that can be used to frame strategies, plans and pieces of analysis on a macro and micro level by wide range of organisations.

How is FinTech currently measured?

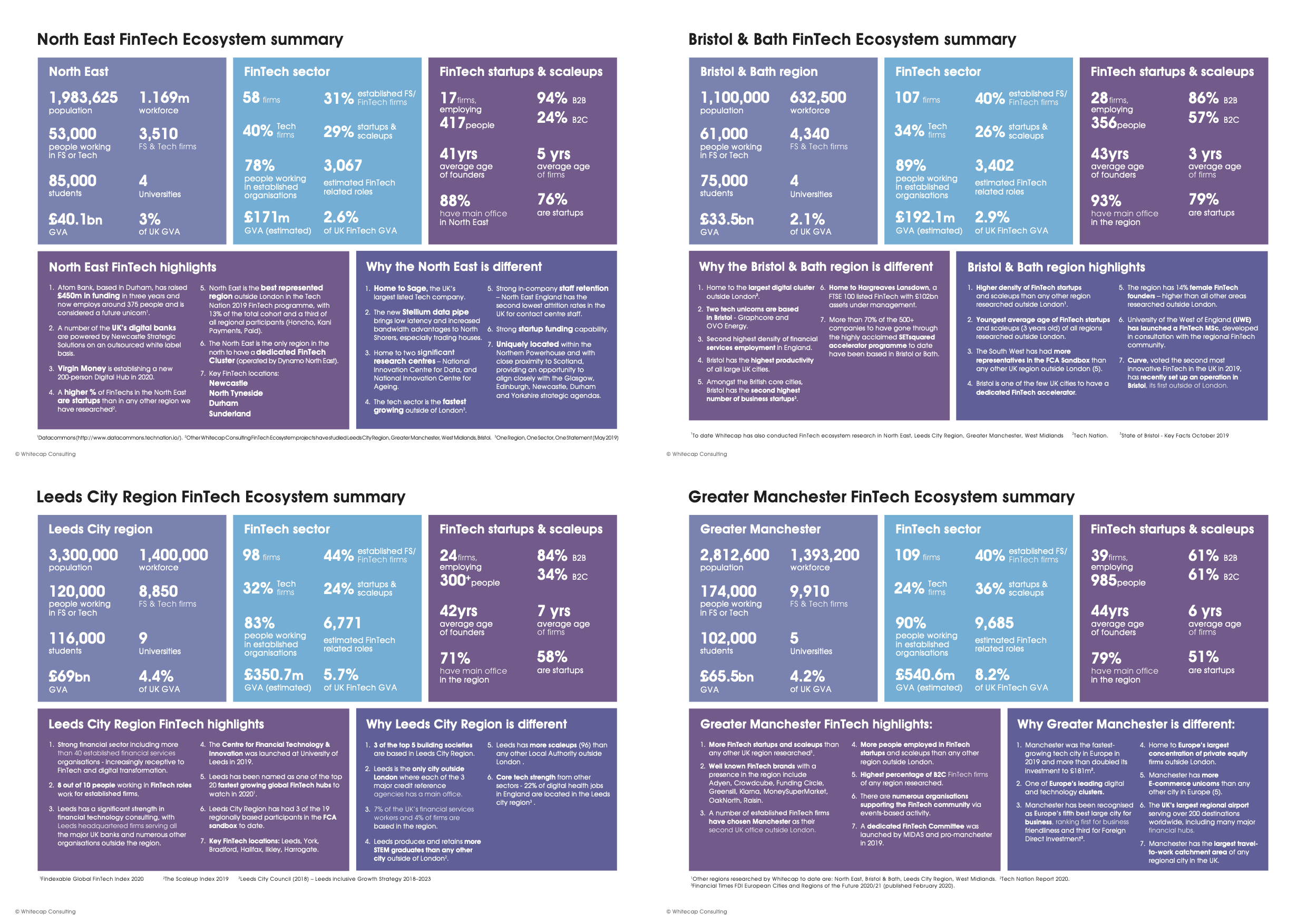

There are some commonly referenced statistics relating to the FinTech sector in the UK, which we’ve listed below. During the course of our regional FinTech research projects – which looked at the North West, Bristol & Bath, Leeds City Region, Greater Manchester and West Midlands – we looked into these numbers and where they came from, so we could work out regional statistics on the same basis. This is what we found:

‘The UK has 1,600 FinTech firms’

- This number comes from the UK FinTech Census 2017, which was published in September 2017. A further Census was published in 2019, with the findings covering key topics such as funding, talent, consumer adoption and international expansion, but the 1,600 number of firms figure was not updated, and continues to be widely quoted from the previous report.

‘76,500 people work in FinTech in the UK’

- This statistic was published in report titled ‘Supporting UK FinTech: Accessing a Global Talent Pool’, in May 2018.

‘The UK FinTech sector is worth £6.6bn’

- The source of this number is an EY report, UK FinTech on the Cutting Edge, published in February 2016. It’s an extensive report, so it seems fair to assume the vast majority of the background research was conducted during 2015.

Over the last year these stats have been regularly referenced in articles, keynote presentations, and in conversation by some of the most senior figures in the financial and FinTech sectors in the UK. It is helpful that everyone references the same numbers, and of course we can all only use the data that is available, but clearly it is far from ideal to be relying on numbers that are up to five years old when this is such a fast changing sector. Consequently, we are certain to be understating the size of a sector that has been identified by Tech Nation as the top preforming part of the UK’s tech industry.

In the process of writing this blog, we spoke to Peter Cunnane, National & International Strategy Lead at Innovate Finance, who said: “There is a clear need for new data, and we will continue to work with various industry groups to support the mapping of the UK FinTech ecosystem. Innovate Finance’s recent visit to Manchester, and time we have spent with other regions in the last few months, has demonstrated that that a more effective mapping of UK FinTech hubs supports local business leaders and politicians as they seek to represent their ecosystem.”

Measuring regional FinTech

When commencing our recent FinTech reports into five key UK regions, we felt it was important that we produced regional statistics to attempt to measure these key areas. We developed an approach to estimate the number of firms, jobs and the value being created in the sector, and we applied this consistently to each region. In developing our approach, we engaged with national policy makers and regional economic development teams.

We do not claim to have developed the perfect solution, but we have shared our approach transparently in our reports and it is outlined below.

The number of firms in FinTech

As the FinTech sector is much broader than startups and scaleups, we decided to measure the firms active in FinTech, rather than firms who can be classed as FinTech.

We identified three types of organisation directly operating within the FinTech sector:

- FinTech startups and scaleups – pure FinTech business models, often with a focus on disrupting the sectors they work in.

- Established Financial / FinTech – established entities, offering financial products or services.

- Tech firms – businesses operating in multiple markets (must include serving financial services or FinTech)

In each region we analysed a combination of desk research, interviews and stakeholder feedback to identify these firms one by one. We also looked at organisations supporting these firms, including advisors, investors and others, but we considered these firms to be the support ecosystem rather than directly operating in FinTech. In addition to feeding this into our analysis, we put all this information into an infographic for each region.

You can see each of our ecosystem infographics and full reports for all of the regions we have analysed here.

The number of FinTech jobs

Categorising jobs within FinTech is also challenging, as it is not the case that everyone working in established financial services or tech firms is working in FinTech, but it is certain that some of them are. If you google ‘how many people work in FinTech in the UK’, the articles on page one results refer to the above mentioned statistics, including one Whitecap wrote in May 2019. There is no recently published data.

We conducted primary research to establish the number of jobs within FinTech startups and scaleups, and used published data from a standard set of sources to ascertain the number of roles in the financial and tech sectors for each region. Subsequently, we adopted a proxy methodology to estimate overall FinTech sector roles.

To calculate the FinTech workforce we adopted the following methodology:

- Estimated FinTech workforce = number of identified workers within FinTech startup & scaleup firms (from Whitecap primary research) + 5% of combined FS workforce (derived from TheCityUK data) and Tech workforce (derived from Tech Nation data).

In the absence of any current publicly available estimate, our 5% estimate is based on a broadening of a previous EY estimate from 2015 (this remains the only estimate published to date) which suggested 5% of the FS sector is categorised as ‘FinTech’. We broadened this to include 5% of the financial and tech sectors – making an assumption that the penetration of FinTech had increased since the previous report, but not having any detailed industry data to work from.

The value created by FinTech

To make an estimate of the value being created by FinTech in each region, we ran a calculation relating to Gross Value Added (GVA):

- Estimated regional FinTech GVA = estimated FinTech workforce X GVA contribution per worker

For the GVA contribution per worker we used the UK average rather than taking regional averages. The UK average GVA is likely to be lower than those working in the FinTech sector generally, but on the basis the skew of London may counteract this, we decided to use the average.

We reported these stats, and various others, via a one page summary which features in each report published.

You can see each of our ecosystem summaries and full reports for all of the regions we have analysed here.

So what next?

The research we have published to date has helped to identify the FinTech activity taking place in what are widely considered to be the five primary FinTech regions in England that are outside London and its immediate vicinity. But London remains the epicentre of the UK’s FinTech activity, and there is also a substantial and increasing amount of activity in Scotland, Wales and Northern Ireland, so the full picture is important to understand. Whilst such an analysis will not necessarily come out of the UK FinTech Review directly, we expect that the review would find this information to be extremely useful and is likely to flag it as a gap in the current knowledge base relating to the sector.

From our perspective at Whitecap, we have done some of the work required and are happy to look at how we can collaborate with others in the UK who have access to complimentary data or insights. Through our direct involvement in two regional FinTech ecosystems (FinTech North and FinTech West) we have an active engagement in the FinTech National Network, an entity which is led by Innovate Finance and is acting as a vehicle to increase communication and alignment of FinTech activity on a regional and national level.

As the UK continues to develop its FinTech capability and invest in the future of the sector, it would be prudent to be able to call on some up to date industry statistics to help the many strong supporters of the sector tell a compelling story on a regional, national and international basis. We’re ready to play our part in helping deliver this over the coming months.

Hopefully you’ve found this article useful. To discuss this topic or how we might support your strategy development and strategy implementation requirements, please get in touch.

Established in 2012, Whitecap Consulting is a regional strategy consultancy headquartered in Leeds, with offices in Manchester, Milton Keynes, Birmingham, Bristol and Newcastle. We typically work with boards, executives and investors of predominantly mid-sized organisations with a turnover of c£10m-£300m, helping clients analyse, develop and implement growth strategies. Also, we work with clients across a range of sectors including Financial Services, Technology, FinTech, Outsourcing, Consumer and Retail, Property, Healthcare, Higher Education, Manufacturing and Professional Services, including Corporate Finance and PE.