Kicking off with the first article, published during UK FinTech Week, Julian Wells, director at Whitecap Consulting, looks at the emergence of FinTech and the opportunities it presents for building societies to better serve their core markets and an increasingly digitally savvy membership.

The recent Kalifa Review stated there are an estimated 2,500 FinTech firms in the UK, of which 81% are made up of less than 50 people, with an annualised growth of 16% vs the SME average of 1.3%.

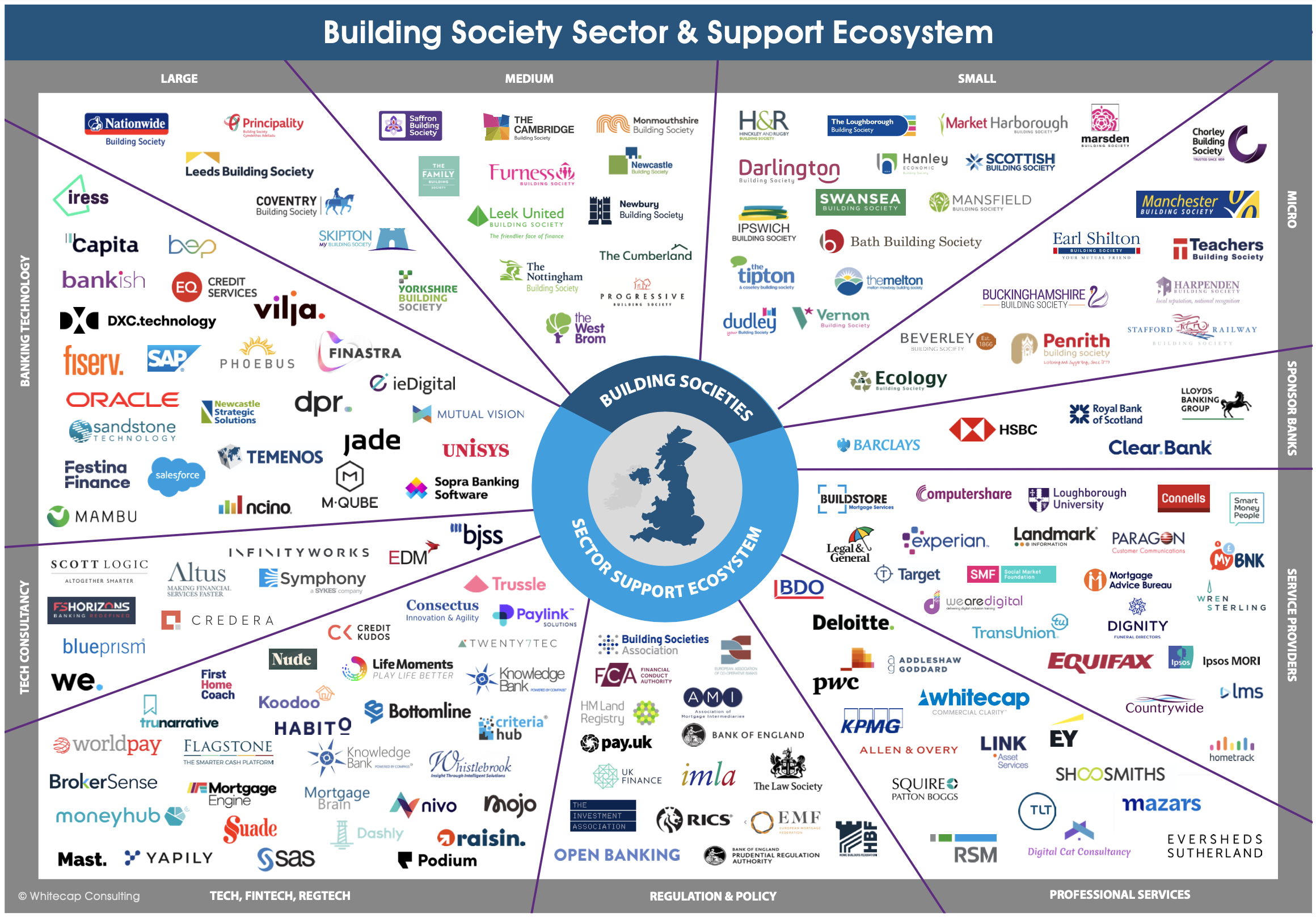

Clearly the FinTech sector is gaining traction as the digitisation of finance continues. Whitecap’s Building Society Sector Analysis report cited around 40 specific FinTech and tech examples from within the sector, which is by no means the extent of FinTech activity being undertaken by building societies. The report also listed more than 60 technology and FinTech firms actively engaged with the sector.

In this article, we highlight four relevant areas of discussion from our report, along with five key recommendations about how FinTechs could improve their engagement with the sector.

In this article, we highlight four relevant areas of discussion from our report, along with five key recommendations about how FinTechs could improve their engagement with the sector.

Legacy systems are a widely acknowledged challenge

FinTech firms innovate and create new ways to deliver financial products, services and processes. They can also help modernise older technology. For the building society sector, legacy systems add a significant layer of complexity when looking at future technology plans with more than 90% of firms relying on legacy technology in some form.

Integrating into legacy systems and adopting a modern, agile, cloud-first approach is a significant challenge for the sector and technology change has been found to be the root cause of 24% of high severity customer-facing incidents.

There are several examples in the sector of societies using Robotic Process Automation (RPA) to handle the rekeying of data into legacy systems, where it has not been possible to put in place data integrations such as APIs.

Where an existing legacy system has no easy way of exposing APIs, smart use of RPA coupled with a middleware API can enable building societies to mirror the benefits of APIs.

Competition to provide FinTech solutions to the sector is strong

Our research highlighted that there are many technology and FinTech firms seeking to work with building societies, and this creates opportunities and challenges for the sector.

CEOs recognise the longer term need to embrace modern ways of working and modern tech provision to maintain their market relevance.

However, the wide range of technology providers to the market presents a challenge when looking to assess their potential future options.

Not least because many do not have the internal resources and knowledge required to identify, plan and deliver significant changes to their technology infrastructure.

Nearly one in three (32%) of building society survey respondents to our research survey stated that the availability of inhouse resource is a key issue with regards to increasing digital capability.

There are also limitations around the appetite to invest in technology, which, when combined with a cautious approach to risk, means the decision-making cycle can be a long one. Within our report we listed some guidelines for FinTech and tech firms aiming to work with building societies:

Suggested actions for FinTech firms seeking to work with the building society sector:

The building society sector is served by a wide range of organisations, and is courted by many more, especially in terms of tech and FinTech providers. During the course of this project, we have identified a number of important considerations for organisations seeking to engage with the sector, and we have articulated these as a set of guiding principles:

-

- Do not assume all societies are the same – take time to understand the nuances of a society’s strategy and business model.

- Acknowledge the impact mutuality has on a building society’s decision making. Products and services that can achieve outcomes such as fast growth, create new revenue streams, or dramatically streamline operational processes can all represent significant changes which may carry significant risk – do not assume these outcomes are more attractive to building societies than stability and sustainability.

- Do not assume that digital transformation is an urgent imperative. Building society CEOs have been hearing this for many years, and whilst they do not deny the importance of digital transformation, the sector does not have the burning platform that some might assume.

- Provide wider context for technology solutions. The tech provider landscape is difficult for societies to navigate, and they are constantly approached by technology and FinTech providers. Helping societies understand where a product or service sits in the market is important to progressing meaningful conversations. Critical factors to consider include compatibility with existing technology and gaps where other solutions will be required.

- Be clear on the requirements you have of a society’s resources. Many building societies are small organisations, with limited resources. If the successful implementation of a product or service requires specific skills or availability, be clear on this from the outset in order to set realistic expectations.

Open Banking is an area of opportunity

65% of all stakeholders we surveyed in our research believe Open Banking to be an opportunity for the building society sector.

Respondents said the largest opportunity from Open Banking lies with enhancing customer experience/ engagement (60%) and data connectivity (51%).

Interestingly, only 13% of building society respondents considered Open Banking to be an opportunity for product distribution compared to 57% of non-building society respondents.

This perhaps reflects the fact that building societies’ established distribution channels perform strongly across mortgages and savings.

FinTech firms we engaged with during the research considered the use of Open Banking by building societies to be at a very basic level, highlighting opportunities for societies to adopt it to help streamline key processes such as ID and verification, dynamic data capture, and the evaluation of mortgage eligibility.

Open Banking will be the dedicated topic of a future blog in this series.

There is distinct FinTech activity around mortgages and savings

Mortgages and savings are the two primary markets for building societies and there are separate streams of FinTech related activity in each of these areas.

Within mortgages, the focus of building societies is to enhance their intermediary mortgage proposition, and many of the FinTech examples in the report focus on engagement with this distribution channel:

- 75% of CEOs interviewed stated that they are seeking to use digitisation to improve their broker journey

- 67% of all survey respondents strongly agreed that technology can drive efficiencies within the mortgage process whilst also supporting the human decision making that is critical to manual underwriting.

In savings, we found building societies are enjoying strong savings performance, which means to date they have needed limited engagement with some of the aggregator / platform tools emerging in the market.

But there is recognition that the saving market could potentially be disrupted and commoditised depending on the combined impact of FinTech and evolving consumer preferences. There are numerous FinTech developments that provide an insight into the direction that the savings market is heading towards.

For example, automated savings goals, round ups, goals, and the ability to have multiple pots within one main account all represent enhanced functionality for consumers. In the short term, the focus of most building societies is to establish an effective online savings capability that enables online account opening and the transfer of funds between savings accounts and bank accounts, but they have more than a passing interest in the direction of travel of the FinTechs in this space.

In summary, the building societies sector is acutely aware that financial services is moving towards a more digital model and that building societies will need to align their ways of working to fit with the way their members and key partners (such as mortgage intermediaries) expect to be able to deal with them.

Deciding which FinTech developments are the most appropriate ones to engage with is a consideration which needs to be aligned to the business strategies and propositions that individual societies decide to pursue.

The related topics of strategy, mutuality and technology are covered in more detail in the report, which you can download the report via the link below.

Background to report:

Building Society Sector Analysis 2021 – A review of the strategic landscape for building societies

The research underpinning the report was conducted by Whitecap Consulting in partnership with the BSA, and involved a quantitative data analysis of all 43 building societies, interviews with 33 of the building society CEOs, and an online survey which received a total of 134 respondents.

This analysis and report was funded through sponsorship from a number of industry stakeholders including: Credera, DPR, EQ Credit Services, Mambu, Moneyhub, Mutual Vision, Nivo, Sandstone Technology, Sopra Banking Software, Shoosmiths, and Phoebus Software.

The eight blogs in this series will focus on key topics addressed in the research: FinTech, Strategy, Mutuality, Regionality, Technology, Mortgages, Savings, and Open Banking.

Useful links:

Building Society Sector Analysis 2021

Watch the report launch webinar