It was in March 2018 when I first spoke to Adam Cox about his new startup, a conference he was setting up to focus on Open Banking, which had officially launched in the UK a couple of months earlier.

It was in March 2018 when I first spoke to Adam Cox about his new startup, a conference he was setting up to focus on Open Banking, which had officially launched in the UK a couple of months earlier.

Adam was intrigued by the regional focus of Whitecap Consulting and FinTech North, and wanted to explore whether there was a partnership opportunity. There was, and later that year, the inaugural Open Banking Expo (OBE) took place in London, with Whitecap and FinTech North as partners. I had the pleasure of chairing the conference, which attracted 300 attendees and 40 speakers drawn from across the UK. We wrote about it here.

Fast forward to 2023 and it was an honour to be invited to chair the main stage for the second day of the conference, and to introduce a line up of national and international speakers. There were some interesting themes coming out of the contributions of the 160+ speakers at the event, which was once again supported by Token as headline sponsor, as it will be next year. I attended the conference with the FinTech North team, which has recently grown to three full time employees (and didn’t have any back in 2018).

This year, the conference was extended to span two days, with over 1,000 industry experts signed up to attend and a stellar line up of speakers. More broadly, OBE has become an international business and runs events in Amsterdam and Canada as well as an active programme of online and broadcast content. The growth of OBE is reflected in the continued increase in adoption of Open Banking in the UK, where it is now used by more than 7 million consumers and businesses.

On the first day I attended various conference sessions and spent time in the exhibitor area. I was struck by two contrasting themes in my conversations. Firstly, the clear opportunity for Open Banking innovation to help the payments sector operate more efficiently and at lower cost; and secondly, the need to protect consumers and businesses against the ever present and growing risk from fraud and financial crime. One panel I listened to was talking about how much faster payments will be able to be made, but then the next panel had a discussion about why it might be necessary to slow some payments down, in order to minimise the opportunities for fraudsters to successfully intervene.

On the second day, the opening keynote on the main stage was from Kate Fitzgerald, Head of Policy at the Payment Systems Regulator. Kate highlighted that innovation can enhance competition, and the UK needs more options than cards, stating that “these options exist but they are not yet perfect.” Kate also highlighted that there are challenges to address in respect of fraud and protection of consumers and businesses.

We heard from Bancolumbia, Columbia’s largest bank, who took part in a fireside chat. Columbia is the 3rd largest FinTech market in South America, after Brazil and Mexico, although 7 out of 10 payments are still made in cash. Interestingly, Columbia is taking a broader approach and starting with Open Finance, not just focusing on Open Banking. Asked what advice he had for the UK market, Luis Miguel Zapata, Vice President of Digital Ecosystems, said he thought we should move faster towards an Open Data model.

We heard from Bancolumbia, Columbia’s largest bank, who took part in a fireside chat. Columbia is the 3rd largest FinTech market in South America, after Brazil and Mexico, although 7 out of 10 payments are still made in cash. Interestingly, Columbia is taking a broader approach and starting with Open Finance, not just focusing on Open Banking. Asked what advice he had for the UK market, Luis Miguel Zapata, Vice President of Digital Ecosystems, said he thought we should move faster towards an Open Data model.

Fittingly, the next session was a panel session on the challenge of striking the balance between openness and protection in the Open Data regulatory framework. Chaired by Sarah Francis of Polymath Consulting, the panel included a familiar face in Janine Hirt, CEO at Innovate Finance, and a key theme was the need to ensure there is value to consumers and businesses in the way data is used. Innovate Finance’s recent FinTech Impact Report found that 97% of UK FinTech firms are having a positive impact on the United Nations’ SDGs.

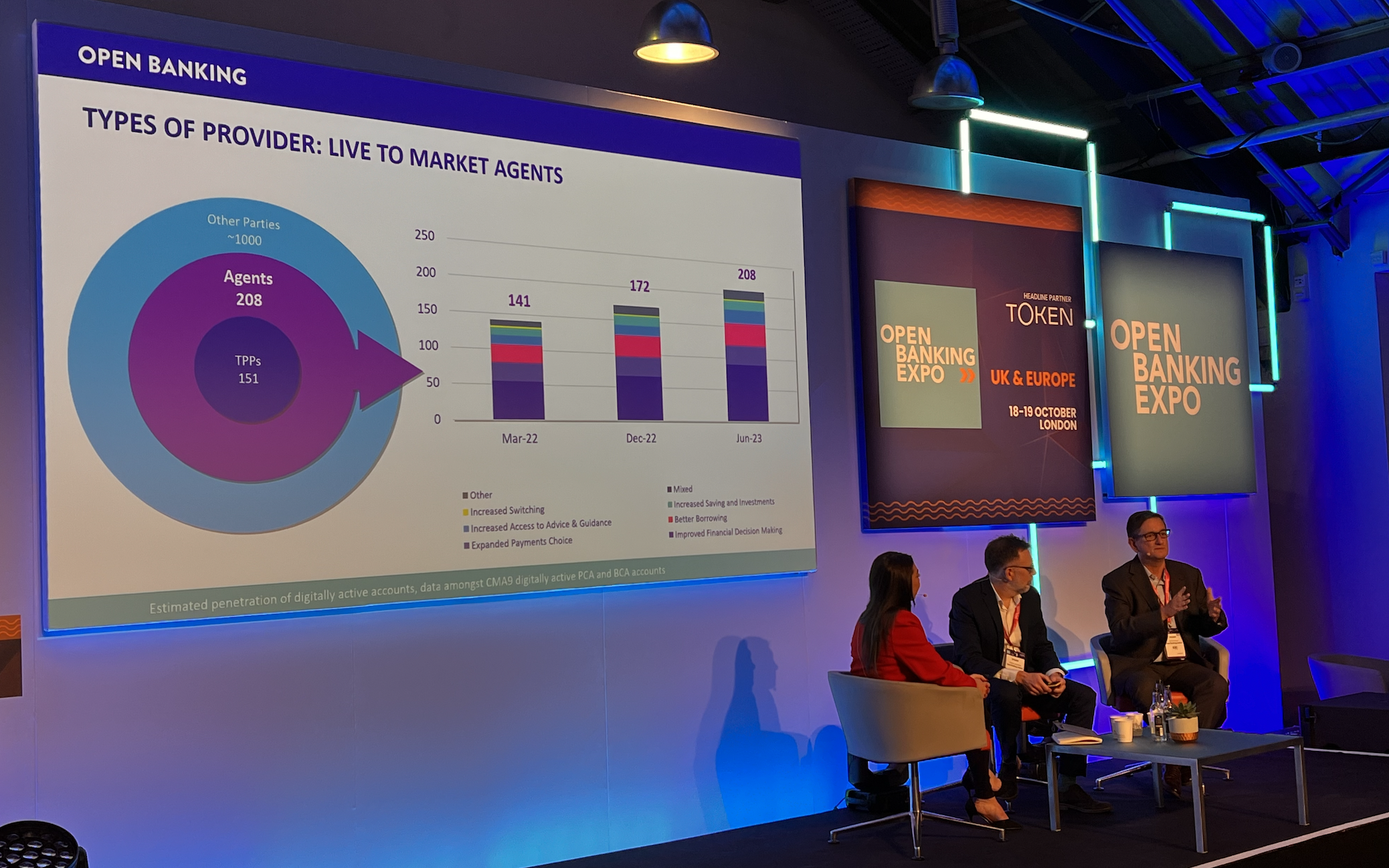

The team from Open Banking ran a session where they reflected on their Open Banking Impact report, which was published earlier this year. reported that they are seeing an increase in FinTech new entrants using Open Banking to provide services related to things such as personal tax management and the collection of invoices by small businesses. It was encouraging to hear that more solutions for small businesses are coming to market, as this was a focus of a major Open Finance report we worked on with Intuit earlier this year. On the subject of Open Finance, there was an entire stream of content dedicated to this subject at the conference this year, with participants including the Centre for Finance & Technology (CFIT), who are currently running a coalition focused on this area.

Tink, one of the most high profile Open Banking brands (which is now owned by Visa), gave an update on Pay by Bank. The session highlighted the importance of making the consumer feel comfortable with the and ensuring the user journey is an easy one. In the UK, it takes 5 clicks and 30 seconds to complete a payment, which is market leading vs other counties. Tom Pope, SVP for Platforms, spoke about the issue of brand visibility during the Open Banking payments journey, and said that Tink is happy to have the entire process take place using the brands of the merchant and the bank, rather than cause any possible friction by using their own brand. It made me wonder whether using the Visa brand would in fact have a positive impact on consumer trust and confidence?

Tink, one of the most high profile Open Banking brands (which is now owned by Visa), gave an update on Pay by Bank. The session highlighted the importance of making the consumer feel comfortable with the and ensuring the user journey is an easy one. In the UK, it takes 5 clicks and 30 seconds to complete a payment, which is market leading vs other counties. Tom Pope, SVP for Platforms, spoke about the issue of brand visibility during the Open Banking payments journey, and said that Tink is happy to have the entire process take place using the brands of the merchant and the bank, rather than cause any possible friction by using their own brand. It made me wonder whether using the Visa brand would in fact have a positive impact on consumer trust and confidence?

We also had a panel focused on regulation, particularly focusing on PSD3 and privacy, also chaired by Sarah Francis from Polymouth Consulting. This panel was summed up perfectly on LinkedIn by panelist Jenna Franklin, Partner at Stephenson Harwood LLP:

“We reflected on the interplay between the payment services and data protection regulatory regimes (PSD2 and GDPR) and how they conflict but also complement each another. We then considered the proposals under PSD3 (due to come into effect in 2026 or thereafter) and how the proposals may present new challenges both specifically with respect to data privacy but more generally for example, the liability regimes as a result of the proposed ‘financial data access’ framework and what practical steps firms can be doing now to mitigate data protection risk. We discussed fraud prevention measures as well as data anonymisation and the increased use of synthetic data to achieve commercialisation of data without the data necessarily being identifiable (either directly or indirectly). We all hope for greater security measures for the consumer, extending refund rights for consumers who fall victim to fraud through an enhanced data sharing environment provided that individuals are aware of how their data is being used and that they have appropriate control over their personal information.”

The future tech panel was chaired by Heather O’Gorman of fscom and included brands such as Uber, Google, Cloudentity and Planky. We heard a lot about data, trust and privacy on this panel, as well as some fascinating thoughts on future innovations. A key message was that getting the commercial model correct is critical.

The NatWest Open Banking team team closed out the day on the main stage with a session focused on the business case for Open Banking, during which they talked through the decision making process and key considerations when looking to buy, build or buy tech solutions. Choosing Open Banking services that are already established in the market is generally the preferred and recommended approach.

We had a slightly earlier finish on the main stage, so I was able to join a panel discussion on the retail stage, where Simon Lyons of obconnect chaired a provocative panel on the topic of ‘What do retailers really think of Open Banking?’ With panelists including Transport for London, Virgin Media, Ordo and Deloitte, it was a great reminder of the importance of retailers and merchants in the successful adoption of initiatives such as Open Banking payments.

As the headline of the blog suggests, my main takeway from the event was the need to balance innovation and positive change with the need to protect against the risk of fraud and financial crime. Giving consumers and businesses the trust and confidence to engage with and use the growing range of Open Banking services must be a key aim over the coming months and years.

Many congratulations to Adam, Kelly, Ellie, Lillie, Lauren and all the team at OBE for an excellent event!