This is the fourth blog in a series about the key findings from my DBA research, which I recently completed at Leeds Business School. These blogs are written primarily for a business audience, and aim to summarise my thesis into a set of concise articles.

This is the fourth blog in a series about the key findings from my DBA research, which I recently completed at Leeds Business School. These blogs are written primarily for a business audience, and aim to summarise my thesis into a set of concise articles.

Overview

The UK residential mortgage sector is substantial, complex, and highly regulated. While FinTech has transformed segments like payments and consumer banking, my research into new entrant mortgage lenders confirms that structural and regulatory constraints are acting as profound barriers to truly disruptive innovation.

If disruptive innovation is defined as the introduction of a product or service that transforms an industry, performing better or costing less than existing offerings, then my study found minimal evidence of its presence. The market overwhelmingly favours incremental technological improvements – streamlining existing processes rather than creating new products or distribution models.

Dual Constraints: Regulation & Legacy Process

The strategic environment for new mortgage entrants is shaped by two powerful constraining forces:

- The regulatory burden: The mortgage market is subject to stringent requirements and oversight:

-

- High barriers to entry: Gaining regulatory authorisation is complex and costly. One founder noted that the requirements needed to run a FinTech startup are “quite different” from what is needed “to run a licensed bank”. This cost and complexity restrict innovation, as demonstrated by the finding that “too much regulation can stifle innovation”.

- Prioritising compliance over creativity: The pressure to comply means resources are systematically allocated toward regulatory requirements and risk management, rather than funding disruptive technologies. This adds complexity and cost.

- The property transaction bottleneck: The primary constraint on deep, transformative change is not the technology of the lenders themselves, but the legacy processes underpinning the entire UK residential property transaction.

-

- Legal process: Founders consistently highlighted that “The legal process is the key issue in the mortgage and wider property buying / selling market”.

- Structural rigidity: Lenders can automate internal underwriting and issue mortgage offers instantly – a key efficiency gain – but the lack of corresponding modernisation in conveyancing, valuation, and legal processes means the overall customer journey completion time remains slow, regardless of the lender’s technology. This structural rigidity limits FinTech’s ability to drive change in core value propositions like speed and price. Broader systemic reforms (particularly to the residential property transaction process) may be necessary to unlock disruptive innovation.

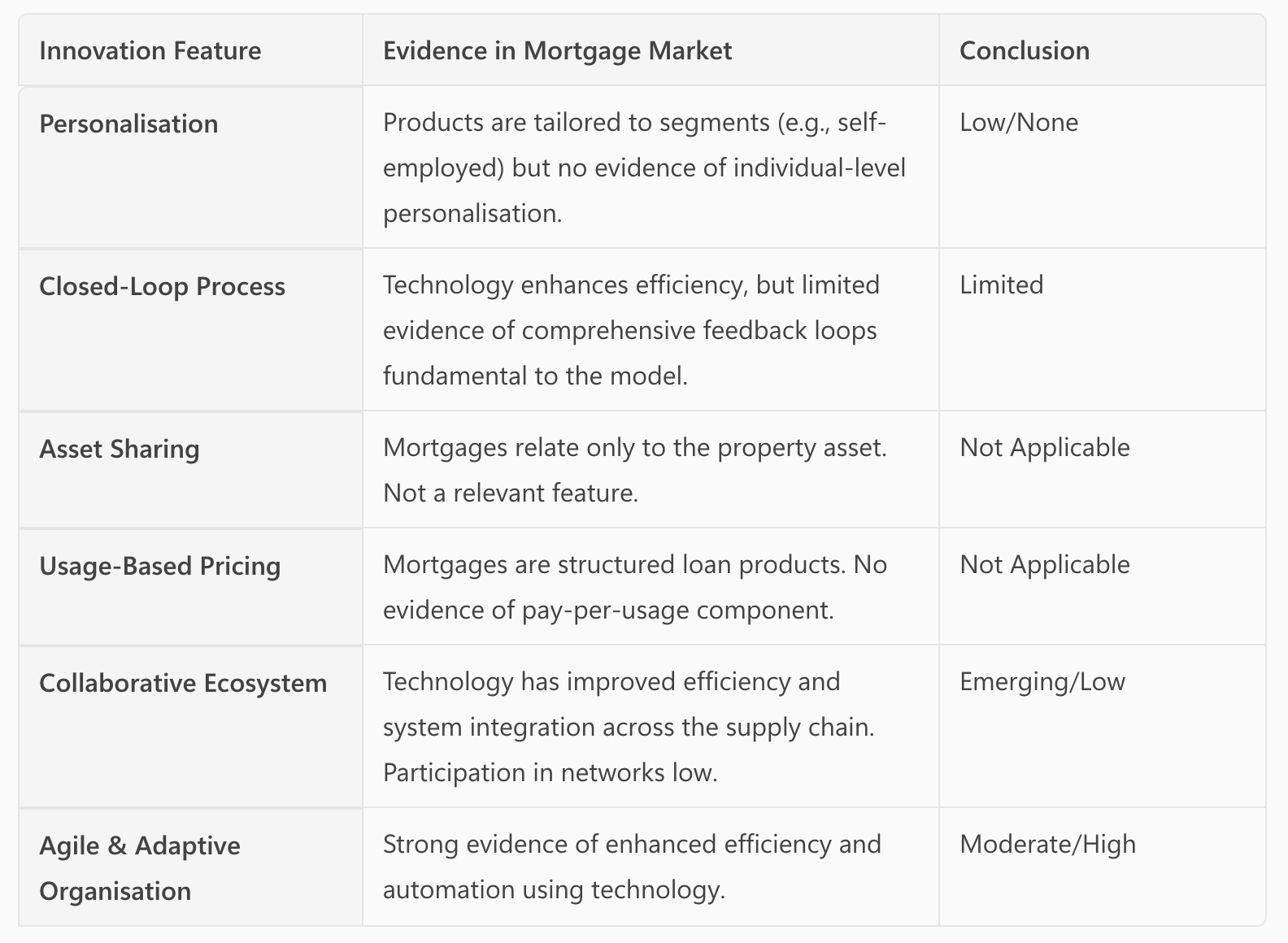

The Absence of Transformative Features

To evaluate the presence of genuine business model innovation, the study applied the framework developed by Kavadias et al (2016), which identifies six features common to successful transformative business models:

Based on this assessment, the mortgage market demonstrates meaningful alignment with only two of the six key innovative features (collaborative ecosystem and agile/adaptive organisation), confirming that business model innovation is not a prevailing force. This suggests the market is structurally resistant to the kind of fundamental change observed in other FinTech sectors.

Based on this assessment, the mortgage market demonstrates meaningful alignment with only two of the six key innovative features (collaborative ecosystem and agile/adaptive organisation), confirming that business model innovation is not a prevailing force. This suggests the market is structurally resistant to the kind of fundamental change observed in other FinTech sectors.

Implications for Policy

For new entrants to move beyond incremental technological gains, systemic change is required. Policy implications emerging from this research suggest that streamlining property transaction processes and addressing regulatory complexity are necessary prerequisites to fully unlock the potential of FinTech in residential lending.

#Strategy #FinTech #Mortgages #Innovation #Regulation

I chose to research this subject areas as they align with my personal areas of interest and expertise. It also reflects where Whitecap Consulting has worked extensively with established mortgage lenders and challenger brands, as well as tech providers, FinTech firms, and other suppliers to the sector, in addition to regulators and trade bodies.

To discuss this blog, my DBA research, or how Whitecap might help you with strategic challenges relating to any of these topics, please email [email protected]

DBA Blog Series:

- Blog 1: Beyond Disruption: Decoding the Strategic DNA of New Entrants in the UK Mortgage Market

- Blog 2: The Driving Force: How Founder Motivation Determines Mortgage Lender Strategy

- Blog 3: The FinTech Paradox: Why Technology Enables Efficiency but Fails to Deliver Lower Prices

- Blog 4: Structural Barriers: Why Disruptive Innovation is Lacking in UK Residential Lending

- Blog 5: The Survive & Thrive Strategy: Specialisation and Service in the UK Mortgage Sector

- Blog 6: Ecosystems: The Missing Collaborative Link in Mortgage Innovation

- Blog 7: The Strategic Motivation Impact Matrix: A New Framework for Financial Services Strategy