In light of the focus on the climate and sustainability, green finance is understandably a hot topic in the financial sector at the moment. Whitecap works across many areas of financial services, and we have observed a marked increase in interest and activity in the mortgage market over recent months, particularly amongst mortgage lenders.

The global growth of green finance

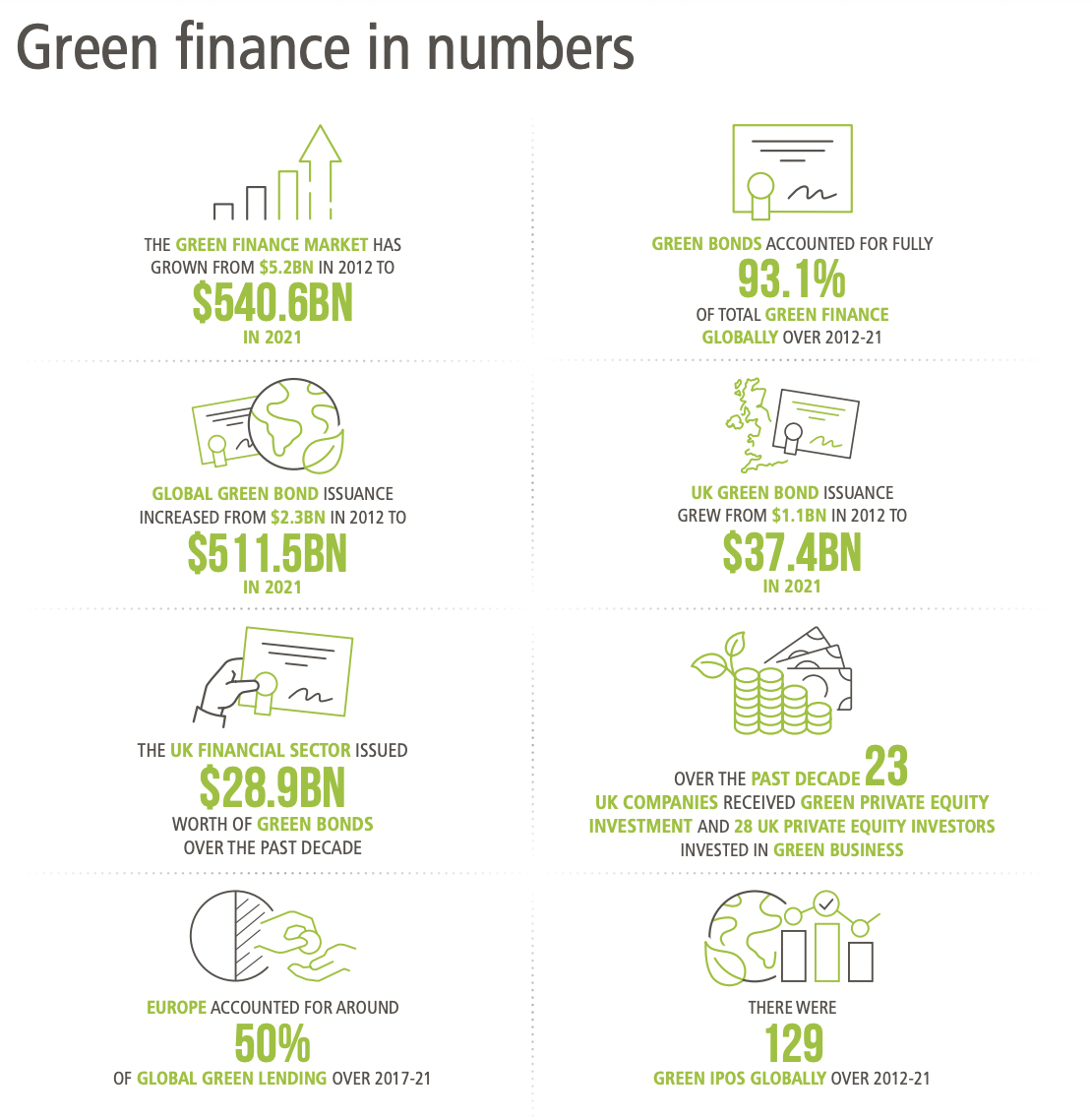

Last month, TheCityUK published a report which included a quantitative analysis of green finance (including green debt and green equity) over a 10 year period (2012-21). It revealed a market that has grown more than ten-fold from £5.2bn to £540bn.

The report claims the UK’s global financial and related professional services ecosystem means that it is well-placed not only to offer the whole range of green finance products and services, but also to demonstrate and promote this proposition through collaboration between the government, financial and related professional services firms, and the wider corporate sector.

Although green finance remains heavily dominated by green bond issuance (93.1% of total green finance), global green lending has grown rapidly since 2017. In the UK, the increase in green loans deals aligns to the government’s target to reduce emissions by 78% by 2035 compared to 1990 levels, and to reach net zero by 2050. Homes will play a big part in this, as the UK’s housing stock accounts for around 14% of all emissions, so the mortgage market has a key role to play.

Green mortgages – the ‘poster child’ of retail banking

In October 2020, the Intermediary Mortgage Lenders Association (IMLA) found that found 74% of lenders expected green mortgages to become a larger part of the wider mortgage market in the future. Their report also found that one in five homeowners said they would be willing to pay an extra £100 a month for a mortgage if it helped to lower their carbon footprint.

Fast forward to 2022, and things have accelerated somewhat, and a report published this month by UK Finance highlights that the mortgage market is increasingly active in green lending:

“Green mortgages have become the poster child of green retail banking products in the UK, but despite their significant growth in the last 12-18 months, significant barriers remain. It is clear that the government considers that mortgage lenders have a key role to play in its strategy to decarbonise buildings.”

Charles Rae, Director, Mortgages, UK Finance

Recent figures from Mortgages for Business show that there were 353 buy to let mortgage products available in March 2022, compared to just four at the same time last year. But there is no standardisation and transparency in terms of features or data, which puts the industry at risk of accusations of green washing, as has been the case in the investment industry.

Across the residential mortgage market, UK Finance’s report observes that green products to date have generally fallen into two categories:

- Green home discount mortgages: incentivising the purchase of energy efficient homes, by offering a discounted interest rate on A or B rated housing.

- Green home improvement mortgage: enables the borrower to borrow money at competitive prices to make energy efficient improvements to their home.

Some new product structures are starting to emerge, and last year Danske Bank launched the UK’s first carbon neutral mortgage. The Carbon Trust certified the mortgage by measuring the carbon footprint of providing mortgages, including the emissions per mortgage generated throughout the mortgage lifecycle. Dankse Bank committed to keep reducing this carbon footprint yearly and to offset any remaining emissions by investing in projects that reduce emissions by the same amount.

Beyond products and pricing

Our recent conversations with mortgage lenders (and their tech partners) have highlighted a clear desire to delve deeper, and to explore new innovations relating to green finance that go beyond product design and pricing.

There is some early activity emerging, with increasing number of mortgage providers creating third-party partnerships to help customers reduce emissions and save money. For example, tools which enable the customer to carry out a home energy check and provide a personalised report and action plan to improve the energy efficiency of their home.

In the examples discussed so far, green mortgages deliver consumer benefits. There are also risks of negative consumer outcomes which need to be mitigated against. For example, it is important to identify and protect consumers and businesses living in older houses who cannot invest in making them more energy efficient. It is possible the supply of mortgages will reduce for these borrowers, effectively excluding them from parts of the market.

So, what next?

We can expect to see an increased amount of regulation relating to the provision of green finance, which will help shape the future shape of the green mortgage market. A report published by EY last year showed that 27% of the UK public feel that by buying sustainably, they are contributing to the future of the planet and society. The stronger the demand from consumers for green products, the more the lender community will accelerate its efforts to deliver these products to the market.

Mortgage lenders have a social responsibility and also a social engineering opportunity in relation to the greening of the mortgage market. They can provide knowledge to support the transition, and can help enable the transition by providing mortgage products.

The mortgage industry has evolved many times in the past and will do so again to adapt to climate change. As with many market changes, this represents a challenge and an opportunity.

Source of image: TheCityUK (March 2022). Green finance: a quantitative assessment of market trends.

If you’d like to discuss this blog post or share your own perspective on the issues covered, please get in touch or comment via our social media channels on LinkedIn or Twitter .

Established in 2012, Whitecap Consulting is a regional strategy consultancy headquartered in Leeds, with offices in Manchester, Milton Keynes, Birmingham, Bristol and Newcastle. We typically work with boards, executives and investors of predominantly mid-sized organisations with a turnover of c£10m-£300m, helping clients analyse, develop and implement growth strategies. Also, we work with clients across a range of sectors including Financial Services, Technology, FinTech, Outsourcing, Consumer and Retail, Property, Healthcare, Higher Education, Logistics, Manufacturing and Professional Services, including Corporate Finance and PE.