It’s widely accepted that the banking sector is undergoing a period of sustained change, with digital innovation, open APIs, PSD2, open banking, and the continued drive for the holy grail of consumer centricity being some of the key drivers.

It is almost universally agreed that the long-dominant big banks will struggle to embrace and adapt to these changes in a timely fashion or on their own and this has created a window of opportunity for so called ‘challenger banks’ to step in and grab market share.

Consumer behaviour and expectations have changed dramatically over recent years, which when combined with a period of limited innovation from established banks has led to the creation of new and innovative completion in the market – the much heralded challenger banks.

Defining the challengers

One of the most challenging things about this sector is to define it consistently, in terms of who is and is not a challenger bank.

So how many challenger banks are there? The answer could be between 19 and 57 depending on who you ask…

Banking Technology listed 57 challenger banks in a list first published in June 2017, which is continually being added to. In contrast, one of the big 4 consulting firms recently shared their definitive list of challenger banks with us, which contained 19 names.

Furthermore, KPMG recently published a report entitled ‘Challenging Perspectives’ which was based predominantly on interviews with the CEOs of challenger banks in the UK, and two of the interviewees do not feature on the aforementioned list of 19.

To further cloud the matter, earlier this year PwC published a report titled ‘Who are you calling a Challenger?’ which referenced a number of challenger banks, including one well-known name that does not appear in any of the lists mentioned above.

Challenger banks or bank challengers?

However one chooses to define the sector, we can agree in principle that it includes any banking product or service provider who is trying win customers from the big banks. Some established banks are also developing or offering challenger banking services, albeit typically under a new brand to compete with the true FinTechs and drive a dual-offering strategy of old world and new world banking.

Interestingly, as not all of these firms are/will be banks, perhaps we should be talking about ‘bank challengers’ rather than ‘challenger banks’.

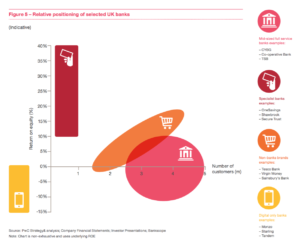

PwC has questioned whether there is such a thing as a challenger bank, breaking the non-mainstream banking sector down into four more distinct segments, and conducting some insightful analysis of their commercial performance:

The inclusion of ‘non-bank brands’ as a category shows the opportunity for challengers to emerge from other sectors where they have strong consumer brands. The likes of Apple, Google, Facebook and Amazon are regularly cited as having a significant opportunity here, and they can be encouraged by the output PwC’s analysis when considering their position vs digital banks.

How can the challengers win customers and market share?

In simple terms the challengers have to deliver customer value.

The key question is not how many challenger brands there are or how we categorise them, but how they are going to woo the customers of their long-established rivals? They will also be competing against each other, not to mention the responses of the mainstream banks who are all looking at how they can accelerate digital innovation and work with FinTech providers to enhance their products, services and processes.

The concept of disruption in banking is widely accepted, although on what scale this will ultimately happen remains to be seen. Views in the industry vary and of course it is usually the challengers making the most bullish forecasts.

“There will be a bank started this decade that will be the size of Google or Facebook.”

Tom Blomfield, Co-Founder, Monzo

The CMAs’ open banking report, published in 2016, highlighted that we’re some way off this promised land at present:

“Older and larger banks do not have to compete hard enough for customers’ business, and smaller and newer banks find it difficult to grow.”

Competition & Markets Authority

As with anything new, the challengers need to have a point of difference or a USP – they need to offer something different to the established banks. KPMG has cited a number of areas of opportunity for the challengers in this respect: customer insight & experience, culture, brand, innovation, and targeted niche product offerings.

Which (if any) of these potential points of differentiation is the most commercially valuable or sustainable is still uncertain.

“Challengers are not merely investing in digital for the sake of digital. They are investing in digital to provide good customer experience.”

Richard Iferenta, Partner & Head of Challenger Banking, KPMG

“Some are starting with the idea that they want to be a cool tech-based digital bank but they don’t have a clear idea of where their customers will come from. Some are more seasoned and understand the customer propositions, and those are the ones I have more confidence in.”

Chris Skinner, FinTech commentator

Digital technology is core to the propositions of most of the challengers, and one of the key differences between challengers and established banks is their approach to omni-channel engagement and access from any device. For example Monzo provides services almost entirely via a mobile app and cash card, and Atom Bank has been very public in saying it is taking a mobile-led approach. Atom has committed to only launch a product or service if it can be delivered via its app. The mainstream banks all offer mobile apps to of course, but often only a restricted selection of services are available via this route.

At Whitecap, we are currently conducting an analysis of over 160 UK FinTech companies and the functions they perform in relation to existing financial institutions. We have found that many of the B2C front end service providers are using very similar language and styles.

So whilst these bank challengers walk and talk quite differently to the banks, they are not doing so well at differentiating from each other. If you’re old enough to remember brands like Cahoot, IF, Egg and Smile then this may all seem rather familiar.

How do the established banks compete?

Whilst the challengers are set to compete on digital and customer experience, the banks themselves have retained a remarkable level of consumer trust in the UK despite the credit crunch and various data security issues.

A recent YouGov report found that 55% of British people trust banks, more than in any of the other European country surveyed (Germany 43%, France 39%, Italy 37%). 67% of British consumers have confidence the banks they use are competent, although only 36% trust banks to work in their customers’ best interests.

The desire to innovate within existing banks should not be underestimated, albeit it can be hard for them to implement at the pace the FinTechs are able to. The example of CYBG (Clydesdale & Yorkshire Bank Group) is interesting and impressive in equal measure. In 2016 CBYG announced it was to invest £350m over a two year period in a new digital banking service called ‘B’, stating it had identified 22 key processes or customer journeys where there was an opportunity to simplify, introduce more automation and digitise.

“B represents a challenge to other banks and, most importantly it’s ready to go now, based around an app that has been extensively tested and trialled – we know it’s what people want. We want to put the fun back into finance and help customers find practical solutions to the challenges they face. Studio B will help people build a better relationship with their money.”

Helen Page, Innovation & Marketing Director, CYBG

As the debate around openness and privacy gathers pace, and cyber security and data protection come more to the fore, the established banks may find themselves better equipped to cope than some of the smaller less well resourced challengers, although that’s not to say that the challengers are not aware of this.

“It is mildly annoying when Uber crashes and you lose a taxi. There’s much more at stake when you make an important transaction. So these new banks know full well how important a reliable service is when trying to convince people to trust a new type of bank with your hard-earned cash.”

Scott Carey, TechWorld

This may well become the key battleground over the next 6-18 months.

So what does the future hold?

Whichever way you look at things it is not going to be an easy ride for the challengers. Metro Bank is generally viewed as the first challenger bank in the UK, and was also the first high street bank for over 150 years. Having launched in 2010 it reported its first profit this year.

According to the Competition and Markets Authority, only 3% of customers with traditional banks switched their personal banking accounts last year. There have also been stories of customers of new banks being asked to close their accounts when they withdrew too much cash, and some of the new banks have lost their licences.

Perhaps the challengers will attract a new generation of customers who have different needs and perceptions and will have no affinity with the banks of today. Or maybe the challengers will end up retaining a focus on niche products and services. Either way the challengers need to find scale and relevance or they will be challenged themselves by innovation in established banks or threatened by new challengers such as Amazon, Facebook and Google.

Over the last 18 months I’ve personally opened accounts with more than one of the digital / challenger banks, although I also cautiously kept my old bank accounts open. Less than a year later I find myself using my old accounts for my day to day banking.

Why? Simply because I can complete the full range of my day to day banking requirements via a standard current account via a suite of services that includes the ability to make contactless payments, direct debits, standing orders, all controllable via a mobile app with no need to visit a branch or even to use online banking. I like the trendy mobile apps and clever marketing of the new banks, but ultimately can’t currently get the same service from any of the brands I’ve tried.

Perhaps I’m not a typical customer but my case study is an illustration of the key issue facing the challengers – namely that there is no compelling reason to switch my loyalty and leave the traditional banks behind.

Without this, large scale disruption in banking risks continuing to be a threat that looms for established banks but does not materialise.

Therein lies the challenge for the challengers.