Since the credit crunch we’ve all seen a few false dawns, but now the numbers over a longer period are beginning to suggest the UK’s return to growth is real. More importantly it also looks sustainable, with the performance looking particularly strong in Yorkshire.

According to the Office of National Statistics (ONS), the UK grew 1.9 per cent in 2013, while estimates for 2014 are even more encouraging. The ICAEW/Grant Thornton UK Business Confidence Monitor (BCM) predicts growth of 1.5 per cent in Q1 2014 alone, claiming it is reasonable for growth throughout 2014 to peak at 3 per cent.

This view is backed up by the International Monetary Fund, which upgraded the UK’s growth prospects for 2014 to 2.4 per cent in January.

These are the ICAEW’s BCM Index highlights:

- Business confidence has risen again in Q1 2014, to a new record high.

- Business performance is strengthening, as annual turnover and profit growth have continued to pick up.

- Alongside higher confidence, businesses are also reporting faster capital investment growth.

- However, export growth remains on hold – a concern given the UK’s trade position.

- Confidence has risen sharply in the Construction sector, pointing to a strong performance in 2014 – encouraging given that output in the sector remains well below its pre-financial crisis peak.

We’ve picked out a few aspects of the report to concentrate on and prepare businesses strategically for what promises to be a good year for the majority in business.

Confident Yorkshire

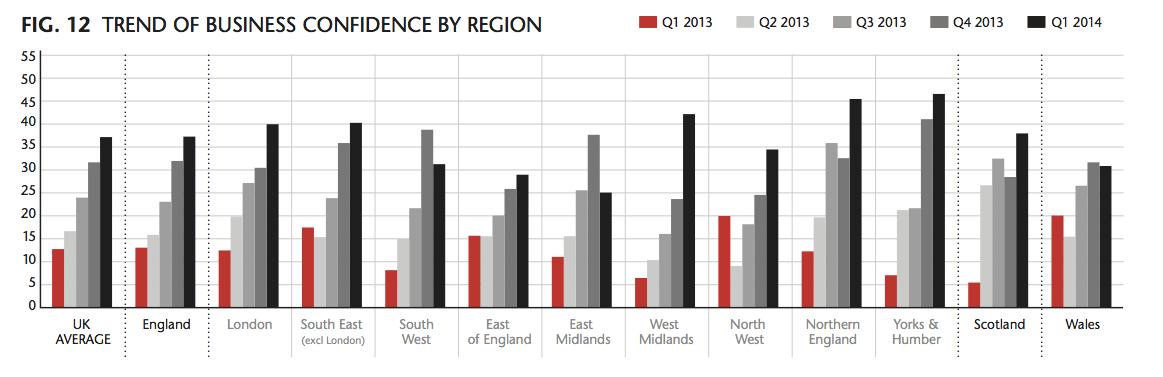

As illustrated in the regional breakdown in the diagram above (Source: BCM), Yorkshire and the Humber is the most confident region for the second consecutive quarter. <click on the chart to see a bigger version>. It has also experienced the most dramatic upsurge in confidence since the start of 2013.

We can speculate on the reasons for this (as the question asked to gauge confidence is simply ‘Overall, how would you describe your confidence in the economic prospects facing your business over the next 12 months, compared to the previous 12 months?’), but planned infrastructure improvements, improving access to finance through new channels like peer-to-peer lending and rising consumer spending in the region’s major cities are sure to have played a part. First Direct Arena and Trinity shopping centre are cases in point.

It is reasonable to expect greater inward investment in the region as firms look to capitalise on events like The Grand Depart and the opening of Westfield in Bradford where major construction work is now underway.

With excellent transport links, lower wages than other areas of the country and an unemployment rate slightly above the national average, operating a business in the region is certainly attractive.

Wage Growth

Companies are already starting to notice the availability of skills as an issue, with a net 14 per cent of businesses reporting non-management skills to be a greater issue than a year ago – the highest level since 2008.

Businesses expect wages to grow 2.2 per cent this year, which would eclipse inflation for the first time since the crisis.

CEOs shouldn’t be scared of wage growth at this rate though.

In line with rising confidence, business financial performance indicators improved in Q1 2014. Turnover and gross profit growth increased, and businesses expect an acceleration in growth over the next 12 months – turnover is projected to rise by 5.5%, while gross profits are estimated to grow by 5.1%.

Impact on Export Companies

Companies looking to export could look forward to greater help from UK Trade and Investment (UKTI) as export values have dropped behind domestic growth. Growth in the UK’s key export markets will not have helped the situation, while increased consumer spending at home may have convinced businesses to concentrate on the UK instead.

The ICAEW’s Index says this ‘raises questions over whether the UK economy will be successful in rebalancing to more trade-oriented expansion’. This will depend on the fortunes of key export and import markets, as well as the UK’s ability to produce more at home and kick its reliance on importing.

China’s dramatic escalation in living standards and consumerism has been reversing the long-term import imbalance, while within the UK; stagnant wages in the last few years have helped to make manufacturing in the UK a more attractive proposition.

Businesses planning an overseas push in the next few years could be in line for a big windfall with the right strategy in place.

Mergers & Acquisitions

Rising business confidence should precipitate a more vibrant M&A environment. Confident CEOs will look to ride the recovery wave as it spills into sustained growth and the right acquisition can be the facilitator for this. Recent research from Cass Business School and Towers Watson showed that UK companies were involved in more mergers and acquisition activity last year than any other country in Europe.

When mergers and acquisitions go well, the new business entity that gets created carries more value than the two (or more) that it was formed from would previously have generated. Of course, confidence can occasionally give way to recklessness and rash decisions (think RBS and ABN Amro…). To make sure a deal turns into a good deal and not an expensive vanity project, it will be important for the businesses in question to stress test their decision making.

__________________________________________________________________________________________

If you’d like to read more on the subject of M&A, our Strategic Due Diligence blogs “How External Strategic Due Diligence Enhances Deal Value” and “How Strategic Due Diligence Drives Post Merger Integration” explore the importance of rigorously testing the rationale behind deals in more detail.