Many will agree ‘FinTech’ is the current business buzz word in the UK, the sector has seen impressive growth attracting global investment and it has brought exciting levels of disruption to the financial services industries. FinTech is the hot sector to be involved in.

What hasn’t received as much attention in the UK however, is the opportunity further afield in the developing world, where FinTech is providing solutions to markets that are not only sizeable, but setting themselves up for these products to provide tangible value for many consumer groups wanting to embrace them. Recent times have seen an increasing number of developing countries embracing the digital age and looking for effective FinTech solutions to solve day-to-day issues unique to developing regions. The widespread growth of mobile phones expanding into previously underserved regions has helped fuel this digital finance opportunity.

Digital finance is becoming increasingly involved in the developing economies, carving out a large market and commercial opportunity. A 2016 McKinsey Global Institute Report highlighted the huge market, economic and development opportunities waiting to be addressed through digital finance. It states; “Through the use of digital finance, some 1.6 billion unbanked people could gain access to formal financial services.”

A convincing case study for this potential market can be seen in M-Pesa, the world’s most successful mobile money service. With over 25 million users predominantly in developing countries, the service allows users to seamlessly send/receive money through a pin secured SMS message to anyone, on any network. Founded in 2007 as a partnership between Vodafone and Safaricom, M-Pesa was initially started as a way for microfinance institutions to more easily collect money from their small loan borrowers. The company observed a much larger opportunity when consumers engaged quickly with the service to start not only paying their microfinance lender, but anybody in their community – whether that was to pay bills, manage agricultural payments or city workers sending money home to their rural families. Now nearly 70% of adult Kenyans use a mobile money account (McKinsey Global Institute Report, 2016).

“Since 2007, M-Pesa has enhanced the lives and livelihoods of people without bank accounts, giving them access to essential financial services through their mobile phones. M-Pesa continues to expand, evolving beyond traditional money transfers to encompass savings and loans, payment of salaries and benefits, settlement of utility bills and school fees and to enable vital health and agricultural solutions”. – Michael Joseph, Vodafone Group Director of Mobile Money.

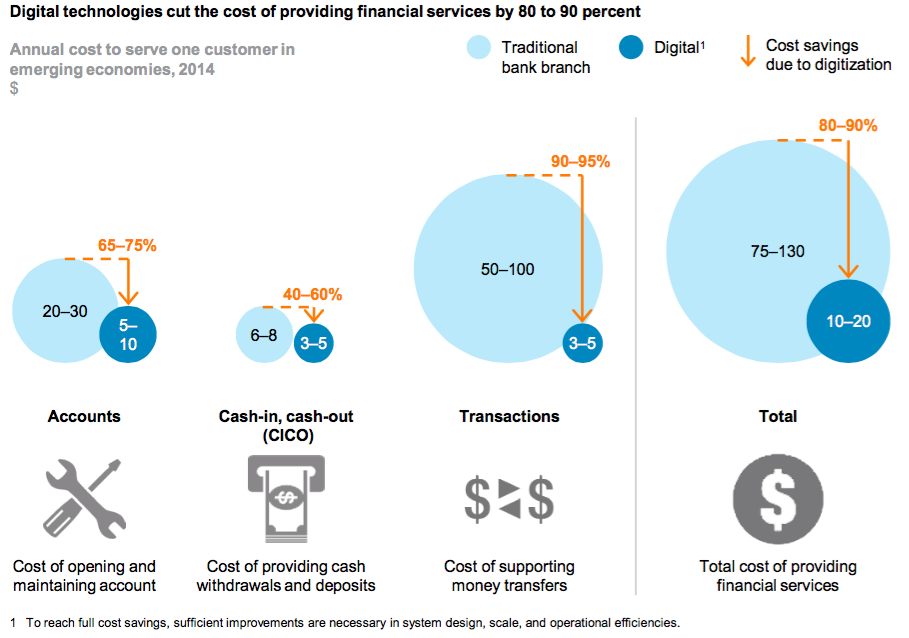

The value these types of products deliver in developing markets is much greater compared to UK customers as it cuts through many social/lifestyle problems these regions face. By providing access and management of finance through digital channels, FinTech products vastly cut costs associated with distributing, handling, storing, and collecting hard cash – this is not only of interest to individual customers from these regions wanting to easily exchange money, but banks, private lenders, and governments. A chart from the McKinsey Global Institute Report below shows the savings digital finance is making in emerging economies.

Combine the huge reduction in operational costs with the fact that many developing countries have citizens without a formal bank account (see chart below) and the value of fintech products jump up even higher – for these people, the ability to store money in digital networks is so useful and valuable such that it becomes their bank. This contrasts UK customers where financial technology products tend to be in compliment to and alongside traditional bank accounts usage. Again here, we see a much greater level of demand and opportunity for digital finance in the developing world.

The opportunities of digitising finance offer multiple benefits and opportunities that providers are moving into, but there is still a huge market still underserved. As beneficial as these products are to developing regions, there are still challenges unique to the ‘developing world’ to overcome.

Infrastructure is a huge consideration for this market as it either fully hinders or provides a complete platform for digital finance innovation. What good is the ability to send digital money if you do not have electricity to charge your phone? Other critical elements for more direct digital finance infrastructure also have to be in place – accepted personal IDs, digital finance payments and mobile phone ownership & connectivity all need to be present for this market to grow.

Further, regulation has had an interesting relationship with Fintech for both developed and developing countries. In the UK we’ve seen regulation playing catch up with recent Fintech innovations. In the developing world however, the lack of strict regulation and allowance for companies like M-Pesa to legally ‘experiment’ has led to rapid growth of beneficial products to millions of people. As digital finance innovation in the developing world continues and more providers move into this space, we can expect regulation to get tighter and the informal ways of transacting/lending money to dissolve. The balance here is for policy makers to cultivate the right business environment where a range of providers can compete on a level playing field and innovative new digital finance products and services, whilst making sure there is sufficient protection and security in place (the continual fight with financial cybersecurity in the UK shows us that even the most advanced tech products come under fire).

We know there is a huge potential in the developing world for FinTech products, both the size and nature of these markets looks attractive to providers. With the success stories of firms like M-Pesa we can see that financial technology is indeed very real and growing in previously underserved regions. The numbers in the infographic below from McKinsey Global Institute report show us the huge opportunity there is for Fintech in emerging economies.

The McKinsey report highlights the immediate opportunity present;

“Capturing this opportunity will require concerted effort by business and government leaders. The rewards are substantial. Rather than waiting a generation for incomes to rise and traditional banks to extend their reach, emerging economies have an opportunity to use mobile technologies to provide digital financial services for all, rapidly unlocking economic opportunity and accelerating social development.” – McKinsey Global Institute Report, 2016.

So we know that there is significant demand, opportunity, and growth in proven digital finance solutions in emerging economies. Further, the UK has invested heavily in developing world-class financial technologies. UK businesses therefore have a twofold opportunity to firstly; learn how financial technologies in some developing countries are leaping forward even without the legacy of an advanced financial infrastructure, and secondly; take UK practice in digital finance solutions and provide them to clients involved in this area – whether that be through the UK private investors in emerging economies, UK public initiatives such as the Department for International Development, the developing world investment initiatives such as the African Development Bank, or the Governments of these countries themselves.

There is an opportunity here to collaborate around FinTech and forge fresh ideas, whilst at the same time developing financial technology solutions to those that need it most. It’s a conversation to start having.

If you are involved in the FinTech sector, you may be interested in Fintech North 2017 event. Hosted at aql in Leeds as part of the Leeds Digital Festival, this showcase event provides keynote speakers discussing topics such as alternative finance, big data and analytics, machine learning and exporting UK FinTech. You can read more details about Fintech North here, or alternatively register here.