Fast forward to 2010 and suddenly it felt like every business operated a cloud model, even if they didn’t offer a centralised, globally accessible, flexible computing infrastructure or application hosting services.

Fast forward to 2010 and suddenly it felt like every business operated a cloud model, even if they didn’t offer a centralised, globally accessible, flexible computing infrastructure or application hosting services.

Over the last 2 years we have seen the latest trend that ‘every’ business needs to be part of – the emergence of EverythingTech. Take the name of your sector, abbreviate it and stick the word “tech” on the end and you are there.

FinTech has been at the for front of this EverythingTech trend, due to significant innovation from start-up businesses, investor funding and the desire to deliver targeted and value adding services that end-users want.

EverythingTech is looking to put the end-user at its heart, deliver value for money, enable seamless integration and data flow between different systems and applications and enable access to everything right here right now. EverythingTech is driven by entrepreneurs using modern technology to disrupt the norm, the drive for higher valuations and ROI, and the aim to deliver innovative products and services.

This is exactly where FinTech has excelled. As banks have found it very challenging and costly to change their products and services, often complicated by legacy systems and processes, that make any innovation difficult, they have struggled to meet the emerging requirements of the millennial generation. FinTech has significantly disrupted this centuries old operating model and is now, underpinned by Open Banking, offering a whole range of innovation to make the life of the end-user easier, such as:

– A single app to combine a user’s current account, savings account and credit cards and to manage finances according to the need of the individual – delivered by Challenger Banks.

– Alternative lending tailored to meet specific needs of borrowers, ranging from capital to operational expenditure, short to long-term – delivered by Peer-to-Peer lending platforms or crowdfunding and facilitated by intuitive lending portals.

– A whole range of new, digitally advanced payment services.

The list is long but the key to FinTech is that it set a trend. Put the end-user first, improve data flows, automate processes, open up your environment to let “outsiders” into your data flow to offer value added services to businesses and end-users in your sector and outside of it. Collaboration is the key word here.

EverythingTech

Now EverythingTech is spreading its wings. We have HealthTech and GovTech, LegalTech and RetailTech, InsurTech and RegTech, Real Estate Tech and TravelTech; though it’s fair to say that some sectors have seen significantly more disruption and value-add than others:

HealthTech is a fast-growing sector including BioTech, life sciences and MedTech. HealthTech start-ups are developing consumer-facing apps to help book NHS appointments, better technology for clinician workflows or even using machine learning to work through genomics data to boost drug discovery programmes.

GovTech has the power to transform public services, achieve better for less and improve outcomes by digitally delivering new services to enable citizens to engage with the public sector and receive the public services they need and by joining up data and services in a mobile, connected world.

LegalTech is disrupting the practice of law by giving people access to online software that reduces or in some cases eliminates the need to consult a lawyer for simple activities, or by connecting people with lawyers more efficiently through online marketplaces and lawyer-matching websites.

RetailTech is seeing significant front-end and back-end disruption, e.g. new flows of real time information, products, transactions and experience, shifting old systems to an omni-channel solution combining EPoS, e-commerce, mail order, supply chain and head-office software. This in turn can help with cash flow, as stock and warehousing can be accurately forecast across the organisation through predictive sales and purchase ordering through to optimisation of all warehousing and distribution.

InsurTech innovations are designed to deliver savings and efficiency from the current insurance industry model including offerings such as highly customised policies and using new streams of data from internet-enabled devices to dynamically price premiums according to observed behaviour. In addition to better pricing models, InsurTech start-ups are driving many new innovations, such as using deep learning trained AIs to handle the tasks of brokers and find the right mix of policies to complete an individual’s coverage. There is also interest in the use of apps to pull disparate policies into one platform for management and monitoring, creating on-demand insurance for micro-events like borrowing a friend’s car.

EdTech, PropTech, MedTech, CleanTech, FoodTech, AgriTech, BioTech, AdTech… the list goes on.

Having considered the Everything in EverythingTech it is prudent to investigate the Tech element and the question arises what Tech actually stands for. Does every sector develop its own specific technologies or are there similarities?

In truth, and to combat any myth that some sectors have developed their own Tech, the technologies used in all these sectors are exactly the same. However, the application of these technologies can vary significantly depending on sector-specific drivers such as regulation, the desire for transparency, customer centricity, requirement to remove cost or to improve efficiency.

To understand sector specific use cases, it is important to cast a light on the underlying advanced technologies that are and will be shaping significant disruption in more detail:

AI (Artificial Intelligence)

The first concern people have with the concept of AI is that the machines will take over. And that is not too far from the truth; however, the question is “take over what?”. Business and end-users are already struggling with the ever-growing data stream that floods our inboxes and communication streams every day and that originate from many different sources and applications. Most of these data streams are operated in isolation without any correlation between them, making it near impossible for us to make sense and arrive at meaningful decisions. We NEED AI to help us make sense of it all, to allow us to focus on the things that really matter and that require human interaction and thinking.

Is a construction business more productive and efficient by investing in a JCB digger or by employing 12 people and giving them shovels? Equally is an insurance broker more efficient by answering 12 calls and going through manual application processes or by enabling an AI driven online portal to fast-track applications and to make some basic decisions as to what insurance products should be offered and which ones should be discarded, before qualified staff can tailor and fine-tune the pre-selected options?

Today AI is making rapid progress and is being used for SIRI, self-driving cars, Google’s search algorithms, IBM’s Watson or autonomous weapons and is designed to perform a narrow task (e.g. only facial recognition or only internet searches or only driving a car). However, the long-term goal of many researchers is to create strong AI that would outperform humans at nearly every cognitive task.

Data Analytics

Data Analytics is the science of examining raw data with the purpose of finding patterns and drawing conclusions about that information by applying an algorithmic or mechanical process to derive insights. There are many use cases, many of which are facilitated by the Internet of Things as explained below.

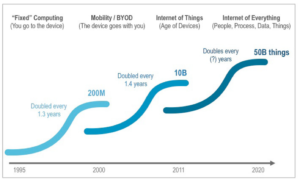

IoT (the Internet of Things) or IoE (the Internet of Everything)

The Internet of things mostly about physical objects and concepts communicating with each other but the internet of everything is what brings in network intelligence to bind all these concepts into a cohesive system. There are many different use cases (as illustrated by Postscapes, a leading IoT resource online), such as:

Infant Monitoring – Aimed at helping to prevent SIDS, the infant monitoring provides parents with real-time information about their baby’s breathing, skin temperature, body position, and activity level on their smartphones.

Medicine Monitoring services are provided via wireless chips that help people stick with their prescription regimen; from reminder messages to doctor coordination.

Activity Level Tracking of a person’s movement and location via a smartphone’s range of sensors (Accelerometer, Gyro, Video, Proximity, Compass, GPS, etc) and connectivity options (3G/4G, WiFi, Bluetooth).

Smart Heating use sensors, real-time weather forecasts, and the actual activity in the home during the day to reduce energy usage.

Smart Bins – Using real-time data collection and alerts to let council services know when a bin needs to be emptied.

Smart Parking – Using sensors, mobile apps, and real-time web applications, cities can optimise revenue, parking space availability and enable citizens to reduce their environmental impact by helping them quickly find an open spot for their cars.

Machine Maintenance – Sensors installed inside equipment will monitor if any parts have exceeded their designed thresholds and will automatically send reports to owners and manufacturers if they have.

Smart Farming combines real-time sensor data from soil moisture levels, weather forecasts, and pesticide usage from farming sites into a consolidated web dashboard. Farmers can use this data with advanced imaging and mapping information to spot crop issues and remotely monitor all of the farms assets and resource usage levels.

Blockchain

A blockchain is a continuously growing list of records, or blocks, which are linked and secured using cryptography. Each block typically contains a record of the previous block, a timestamp and transaction data. By design, a blockchain is inherently resistant to modification of the data. It is an open or distributed ledger that can record transactions between two parties efficiently and in a verifiable and permanent way. Once recorded, the data in any given block cannot be altered retroactively without the alteration of all subsequent blocks, which requires collusion of the network majority.

The most popular use case for blockchain is crypto-currency with Bitcoin being the world’s first permanent, decentralised, global, trustless ledger of records. Since its invention, entrepreneurs in industries around the world have come to understand the implications of this development because the idea can now be applied to any need for a trustworthy record. It is also putting the full power of cryptography in the hands of individuals, stopping digital relationships from requiring a transaction authority. Key use case are as follows:

– Financial Services – There are several key use cases for financial services, such as providing an infrastructure for cross-border transactions, governance and markets, regulatory reporting and compliance, clearing and settlement as well as accounting and auditing

– Identity – With Blockchain there is no need to build a new identity infrastructure, as several ones already exist that use open Blockchain to store the identity details. Anyone who wants to verify just has to query the open Blockchain

– Notary – Most ownership records are stored in paper ledgers. These can be tampered. The data on Blockchain cannot be altered.

– Digital Assets – ICOs (Initial Coin Offering) is a new way to raise investment. Anyone anywhere can now become an investor. ICOs offer a digital asset called token. These tokens will be stored in a Blockchain wallet and these tokens can be used to pay for services or exchanged a later date when its value increases.

– Smart Contracts digitally facilitate, verify, or enforce the negotiation or performance of a contract. Smart contracts allow the performance of credible transactions without third parties. These transactions are trackable and irreversible.

– Digital Voting – The biggest problem with online voting is its security. Votes can be tampered with or hackers can find out who a person voted for. Blockchain can make the vote anonymous and provide better security. Since voter turnout is often low, digital voting can bring in more participants.

– Distributed Storage – Presently people use services like Gdrive, Dropbox to store files. The problem is they have to trust these providers with their data. Governments can force them to disclose data if required. On Blockchain data is decentralised its stored on different computers on the network with high encryption.

Now imagine one or several of these advanced technologies being used within specific sectors, and in collaborative models across different sectors, which brings us back to the concept of EverythingTech.

It is not a coincidence that the medium that has facilitated these truly game changing Techs, i.e. the Internet, has already showed us the way. First there was the Internet, which is slowly transforming itself into the Internet of Things with the future being the Internet of Everything.