In this blog we focus on Green Finance, an area of growing importance as the sector supports the UK’s transition to net zero. This chapter was sponsored by fintechOS.

Chapter Summary: Green Finance

There has been notable growth in green finance, particularly within the mortgage market, with building societies developing a range of innovative products to support environmentally sustainable housing.

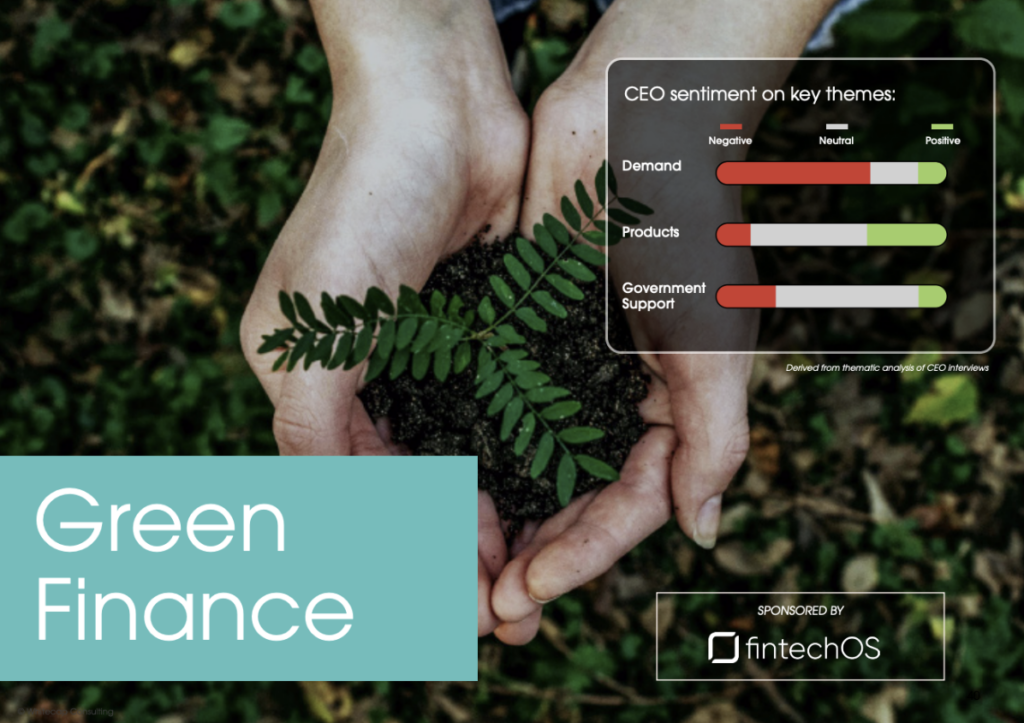

However, despite product availability, both demand and consumer awareness remain low. This has resulted in limited uptake of retrofit and green finance products.

Sector Role in the Net Zero Transition

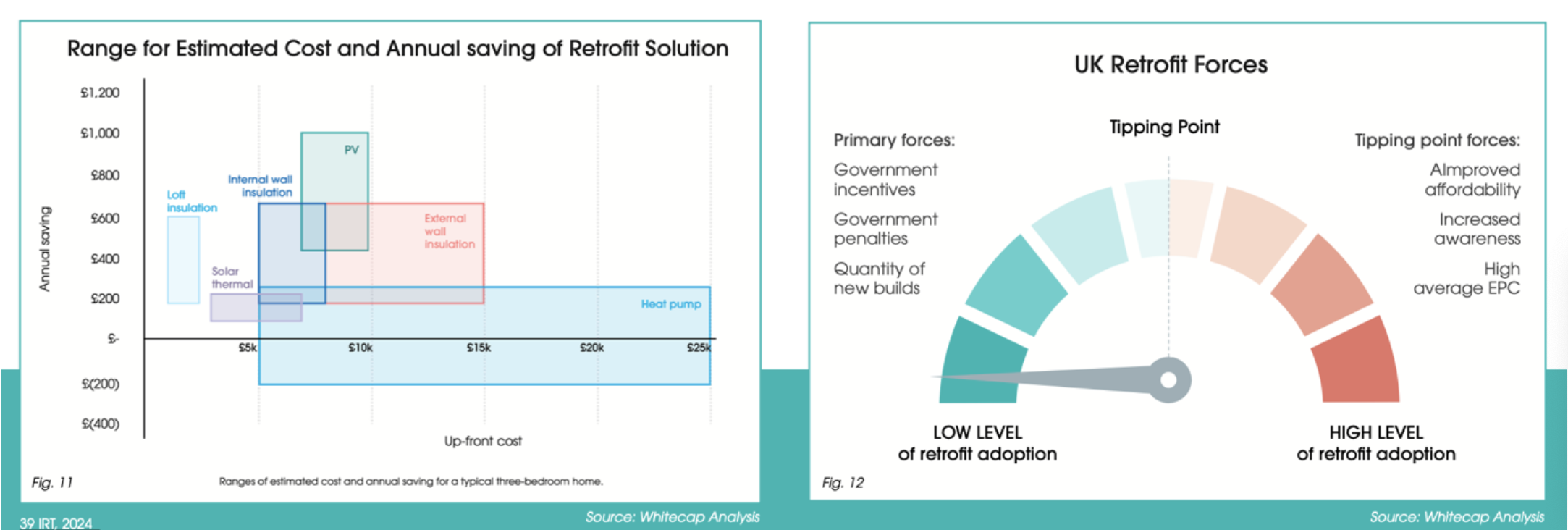

Building societies recognise the opportunity and responsibility to contribute to the UK’s carbon reduction targets. Their long-term perspective and community focus position them well to support members in improving the energy efficiency of their homes. At the same time, the report finds meaningful growth in green finance and retrofitting will require stronger government support, both in terms of policy direction and financial incentives. Currently, the support available is seen as insufficient to drive the scale of change needed, as illustrated in Figure 11 below.

Mark Selby, CEO of Hanley Economic Building Society, provided an example to highlight the issue:

“The cost of getting a house from an EPC rating of D up to a B can be greater than £60,000. That’s beyond the reach of most people and I think it’s a big challenge in terms of the impact on the value of the property versus the investment required.”

Challenges in Implementation

A key issue is the lack of standardisation in green mortgage products. Definitions, eligibility criteria, and metrics vary, making it difficult for consumers to compare offerings and for societies to scale solutions. There is a strong call for industry-wide frameworks and data standards.

Consumer Engagement and Incentives

Consumer awareness and demand for green finance remain modest. Many homeowners are unclear about the benefits or costs of retrofitting, and limited government incentives present a further barrier. Building societies are exploring ways to raise awareness, offer tailored advice, and incentivise green improvements.

Graham Lloyd, Strategy Director at Nationwide, said:

“We’ve got a 0% Green Additional Borrowing mortgage. We’ve seen a slight increase in take-up off the back of some publicity, but it’s very modest.”

Richard Ingle, CEO of Bath Building Society, also reported a degree of interest:

“There is some demand for green products. Members are seeking advice on how to improve the energy efficiency of their homes.”

Data, EPCs and Risk Assessment

Accurate, accessible data is essential for evaluating property energy performance. Current EPC ratings are often outdated or inconsistent, and societies need better tools to assess retrofit potential and climate-related risks. This is crucial not only for product development but also for managing portfolio exposure.

Long-Term Strategy and Innovation

Societies are starting to embed green finance into broader strategy, viewing it not just as a compliance issue but as a business opportunity. Innovations include linking green mortgages to discounted rates, funding retrofit pilots, and collaborating with fintechs to develop more robust environmental criteria.

Encouraging Market Transformation

As early adopters, building societies have a chance to lead by example. By investing in green innovation and advocating for policy support, they can accelerate the development of a sustainable housing market that benefits members and the environment alike. Some societies are investing in developing their own green finance case studies, to help bring the concept to life for consumers.

Peter Burrows, CEO at Cambridge Building Society, was one of several chief executives to share an example:

“We have bought a three-bed semi-detached house, and we are completely redeveloping it to make it as green as possible. We’re going to be completely open about how much we spent, the environmental impact, and the difference it’s made to the bills.”

What next?

Green finance has enjoyed a high profile but significant consumer demand is still to materialise. Purpose-led organisations such as building societies are well placed to champion green finance in the mortgages and savings space, which would align well with their core purpose of being member-focused. While the global direction may have shifted away from green initiatives following political changes, building societies are uniquely positioned. They are not driven by shareholder demands, allowing them to make long-term decisions that benefit their communities and wider society.

This is Blog 6 in our nine-part series covering the Building Societies Report 2025. You can explore the full series here:

- Blog 1: Strategy & Mutuality

- Blog 2: Mortgages

- Blog 3: Savings

- Blog 4: Branch of the Future

- Blog 5: Homebuying Process

- Blog 6: Green Finance

- Blog 7: Diversification & Collaboration

- Blog 8: Technology

- Blog 9: Regulation, Policy & Risk

The Building Societies Report 2025 was created in partnership with the Building Societies Association and made possible by the support of sector sponsors including: BJSS, Digilytics, Finova, FintechOS, FIS, GDS Link, Mambu, Mast, Monument Technology, Mutual Vision, MQube, nCino, Ohpen, PEXA, Phoebus, RSM UK, SBS, Target Group, Temenos , Unblu, Unisys, and Vilja Solutions.